6 Answers to Pressing Questions with Talley Léger of The Wealth Consulting Group

2025 has delivered no shortage of headlines, ranging from sharp rotations in equity leadership to macro surprises that forced investors to reassess their positioning. As the year winds down, we sat down with Talley Léger, Chief Market Strategist at The Wealth Consulting Group (WCG), to get his perspective on how markets are setting up for 2026 and beyond.

Léger brings more than 25 years of experience across some of the industry’s most respected research organizations, including senior strategist roles at Raymond James, Invesco, Barclays, Merrill Lynch, and RBC Capital Markets. His insights have appeared in Bloomberg, Barron’s, The Wall Street Journal, MarketWatch, CNBC, and other major financial outlets.

This fall, Léger and WCG’s Investment Strategy Committee published Small Cap, Big Picture: A Major Turn in the Size Cycle, a research outlook examining the conditions that may drive a renewed size-cycle shift. To build and analyze the visuals behind that outlook, Léger used YCharts’ historical datasets, macroeconomic indicators, and charting tools, which helped him illustrate the valuation, earnings, and financial-conditions trends featured in his work.

In the conversation below, Léger discusses what collapsing consumer sentiment may signal for future equity returns, how technology’s 2025 leadership fits into the broader regime, and what easing rates, tighter spreads, and a calmer volatility backdrop could mean for market participation heading into 2026. He also brings some of the charts that powered his research, so you can recreate the analysis directly in YCharts.

Q&A with Talley Léger

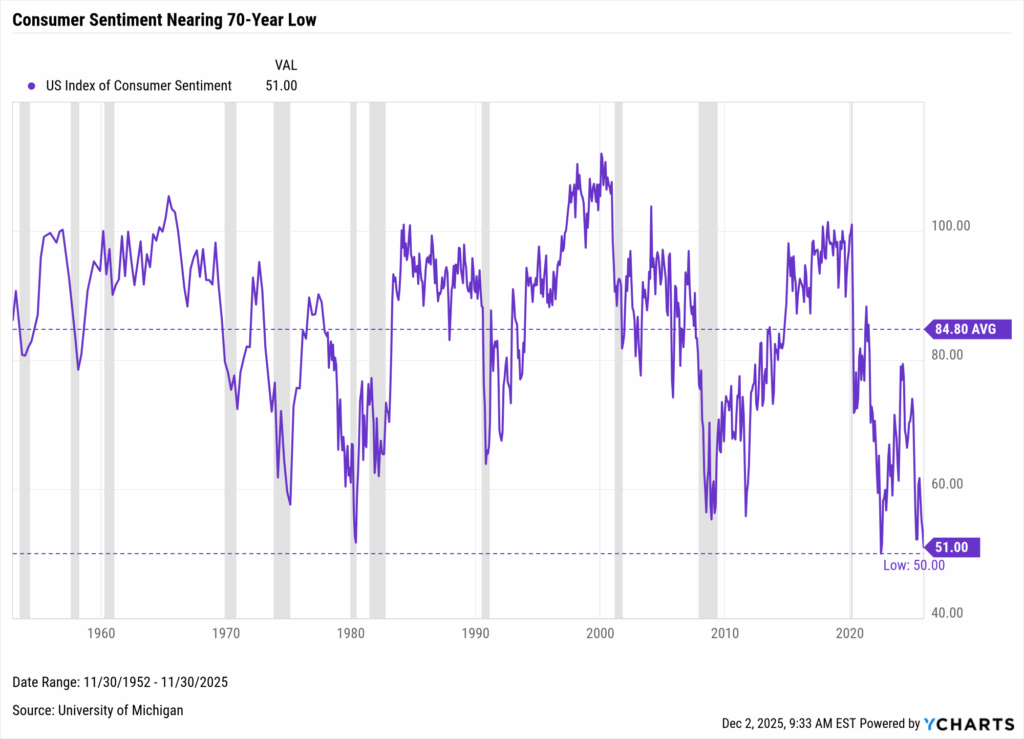

YCharts: Consumer sentiment has fallen to one of its lowest readings since the 1950s, even as equities continue to climb. How do you interpret that gap between how households feel and how markets behave?

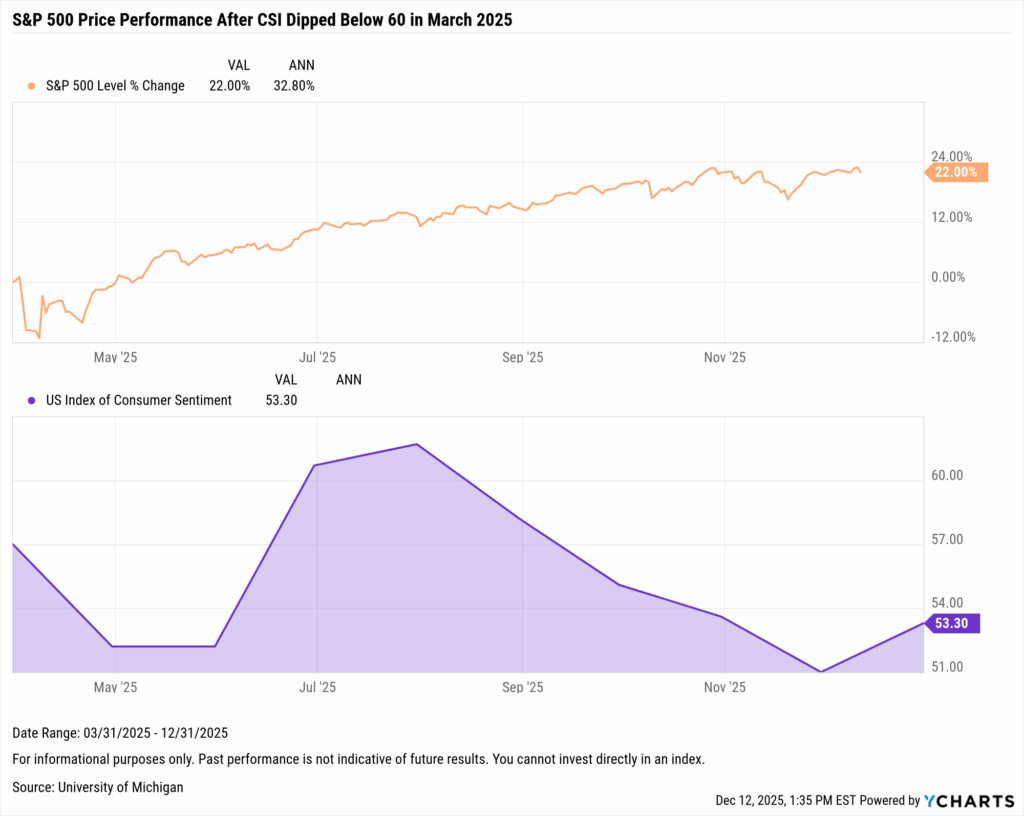

Recreate in YCharts | Recreate Overlaid with the S&P 500

Talley Léger: Understandably, households are generally worried about the potentially negative, albeit temporary, economic consequences of the longest federal government shutdown in history. According to the Conference Board, consumers are also saying that jobs are increasingly hard to get. Moreover, lower-income Americans with few or no assets have been left out of the rally.

However, our research shows that the median rolling 12-month forward return on the S&P 500 – from Consumer Sentiment Index (CSI) readings less than 60 – was a whopping 18% since 1973! Furthermore, the success rate, or frequency of positive returns from that strategy, was a lofty 88% (21 out of 24 instances). As Sir John Templeton said, “Bull markets are born on despair.”

Since March 2025, when the CSI fell below 60, US large-cap stocks have produced a compound annual growth rate of almost 29%! It pays to be bullish, in our view.

YC: Technology has once again been a dominant force in driving returns this year. In your view, does that leadership look sustainable, or are you watching for other parts of the market to assert themselves in 2026?

TL: Investor concerns about rich valuations, high concentration, and narrow participation in the tech sector are valid. However, The Wealth Consulting Group’s cycle-on-cycle analysis shows that tech stocks ballooned 925% from the release of Netscape Navigator 1.0 to their peak in March 2000. Since the launch of ChatGPT, tech stocks have risen just 156%, a comparative shortfall of 769%.

While risks are rising, they still don’t compare to the late 1990s. If past is prologue, tech stocks may have plenty of room to run, especially if investors stay willing to pay up for strong sales, high margins, and robust earnings growth. In our view, it’s too soon to expect a tech stock crash. Rather, we see a catch-up phase for the rest of the market, including small caps, powered by technological innovation. In other words, technology itself should enable a broader, healthier market.

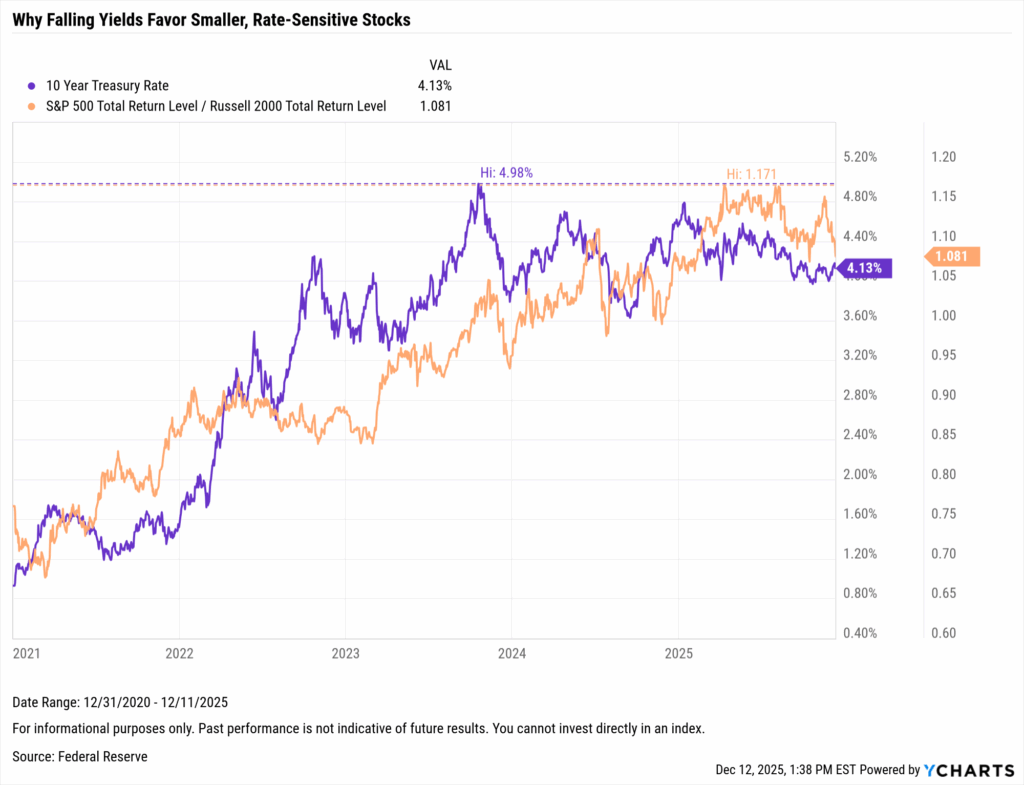

YC: Interest rates have been drifting lower as the Federal Reserve (Fed) eases. How is this shift in the rate environment influencing the market’s risk dynamics in your view?

TL: True, nominal and real interest rates have softened alongside a dovish Fed. 10-year US government bond yields have eased to the benefit of riskier, less-liquid stocks with higher shares of variable-rate debt, namely small caps.

Favorable rate dynamics are among the numerous catalysts we see unlocking the potential reward embedded in smaller company share prices. Fed interest rate cuts, a positively-sloped yield curve, improving lending standards for small firms, and an upswing in small business optimism are positive agents of change that should fan the flames of recovery for small caps.

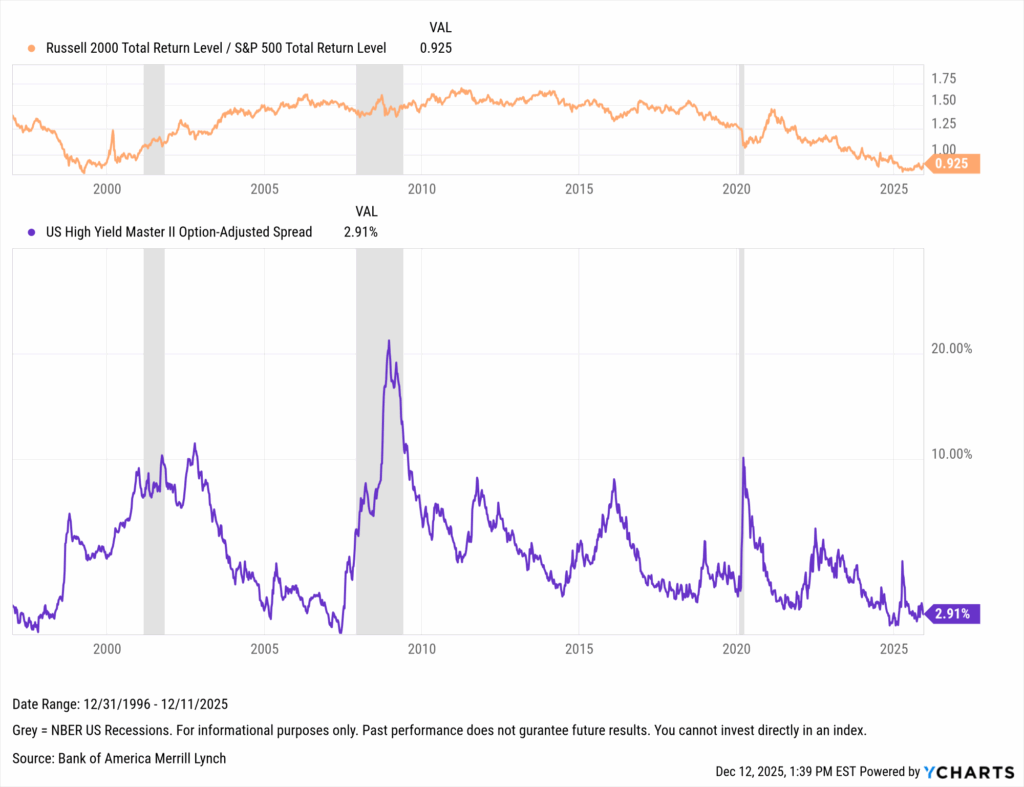

YC: We’ve also seen meaningful tightening in credit spreads. What does that tell you about investors’ willingness to take on risk?

TL: Right, the below investment-grade cost of capital has fallen relative to its investment-grade counterpart. In short, quality spreads have narrowed, suggesting that investor risk appetite is healthy. That’s important because credit is the lifeline to smaller firms, and crucial for keeping their growth “promise” to investors. When the spread between below investment-grade corporate bond yields (or borrowing costs for risky businesses) and those of their investment-grade counterparts is wide (so-called quality spreads), investors demand high compensation for taking risk. In 2025, however, investors have required a modest premium for risk-taking. In our view, small-cap stocks are a buy because the credit cycle continues, and we already experienced a major credit event (i.e., the 2023 regional banking crisis).

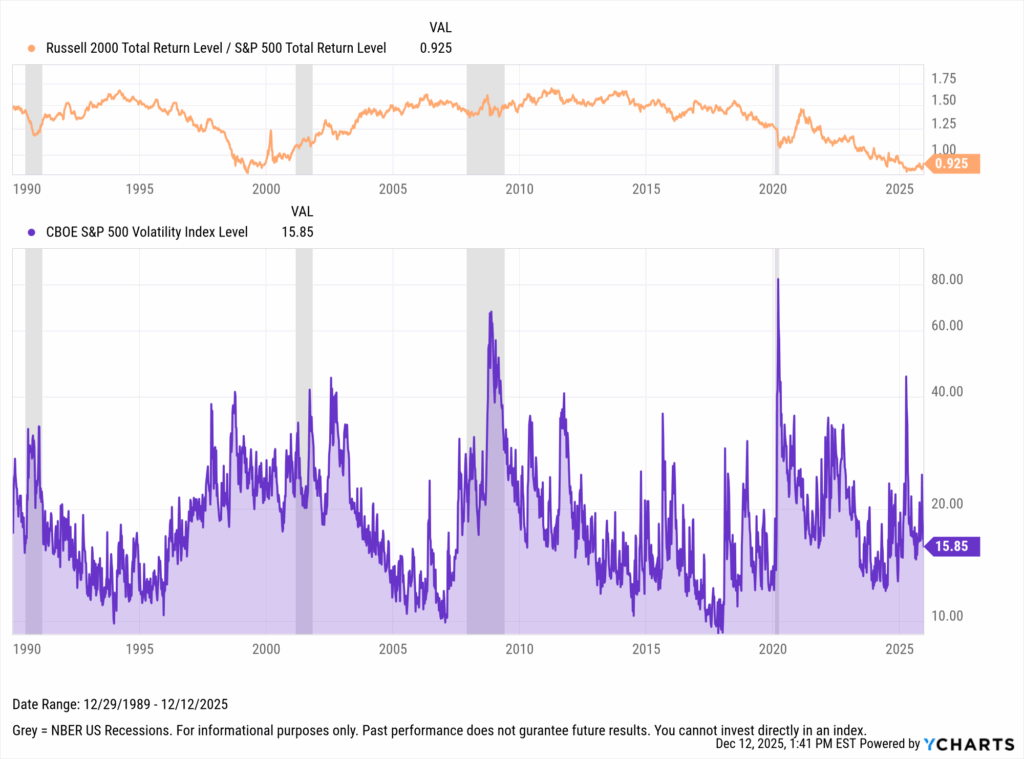

YC: Equity volatility has settled back to calmer levels from early 2025. How influential is a lower-volatility regime in shaping where capital flows next?

TL: Yes, declining volatility has supported riskier, less-liquid stocks. The Chicago Board Options Exchange (CBOE) Volatility Index (VIX) – the so-called “investor fear gauge” – is a real-time financial market proxy for investor sentiment and risk tolerance. Generally, volatility trends are negatively correlated to the relative performance of small caps.

In other words, the outperformance of the Russell 2000 (small, high-growth companies and riskier, less-liquid stocks) vis-à-vis the S&P 500 (big, stable, high-quality companies and liquid stocks) makes sense in the context of diminished fear in the marketplace. This cycle, ebbing stock market volatility has supported small caps. Keep calm and carry on, folks.

YC: When you put all of this together—weak sentiment, easier rates, tighter spreads, and lower volatility—what kind of market participation do you see ahead in 2026?

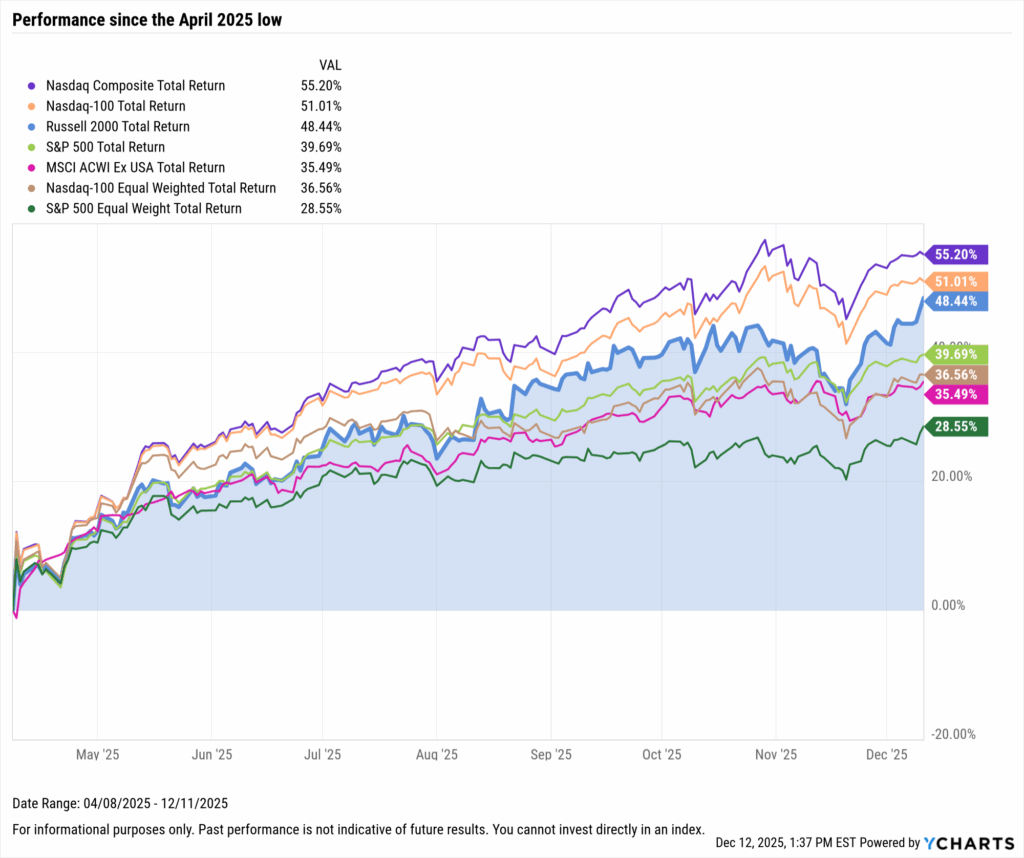

TL: Since early January, WCG’s Investment Strategy Committee (ISC) has expected a double-digit stock market return led by the pro-cyclical, economy-sensitive sectors, namely information technology and consumer discretionary. Lo and behold, the surge in those sectors since the April low has ratified our risk-on portfolio posture.

If the mid- to late-1990s are the blueprint for tech mania 2.0, US mega-cap tech stocks should maintain a dominant share of investors’ portfolios. Strong fundamentals may remain the key drivers of tech stock performance, which is why we’re staying overweight and why we expect the sector to spur another 20% gain on the S&P 500 to ~8,500 -/+ in 2026.

Elsewhere, the size cycle may be turning like it did before the Dot.com bubble burst in 2000. We think of small caps as an underappreciated way of diversifying or mitigating growing concentration risk in mega-cap tech stocks.

As discussed, the setup and timing for small caps are compelling:

- Valuations are unusually attractive

- Earnings may be poised for a powerful recovery, supported by an economic re-acceleration

- Interest rates are softening

- Corporate bond spreads are well-behaved

- Volatility is relatively calm

- The technical backdrop supports a potential inflection point at a historically meaningful level (1998/1999).

The bottom line is we remain bullish on risk assets in general and stocks in particular as long as earnings rise, interest rates fall, and books about market crashes (1929) make the bestseller’s list.

Bridging Research and Client Conversations in 2026

As 2025 closes, Talley Léger’s perspective highlights that investors may be entering a regime where participation widens and new opportunities emerge beyond the familiar giants.

For advisors and research teams alike, staying ahead in this environment requires tools that make it easy to visualize trends, test narratives, and translate complex insights into client-ready conversations.

YCharts brings those capabilities together, helping investment teams elevate their research and seamlessly empower client-facing advisors with clearer, faster, and more actionable analysis to better serve clients.

Whenever you’re ready, here’s how YCharts can help you:

1. Looking to Move On From Your Investment Research and Analytics Platform?

2. Want to test out YCharts for free?

Start a no-risk 7-Day Free Trial.

Disclaimer

©2025 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts”) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure

Next Article

Monthly Market Wrap: November 2025Read More →