Explaining the Blue Owl Headlines to Clients

Executive Summary: Blue Owl’s recent loan sale and redemption halt have reignited comparisons to 2007, but the core issue appears to be liquidity structure rather than widespread credit deterioration. The episode highlights the tension between semi-liquid fund features and inherently illiquid private loans, prompting investors to reassess valuation governance and redemption terms.

The Blue Owl headlines are not about a sudden collapse in credit fundamentals. They are about liquidity mechanics inside semi-liquid fund structures.

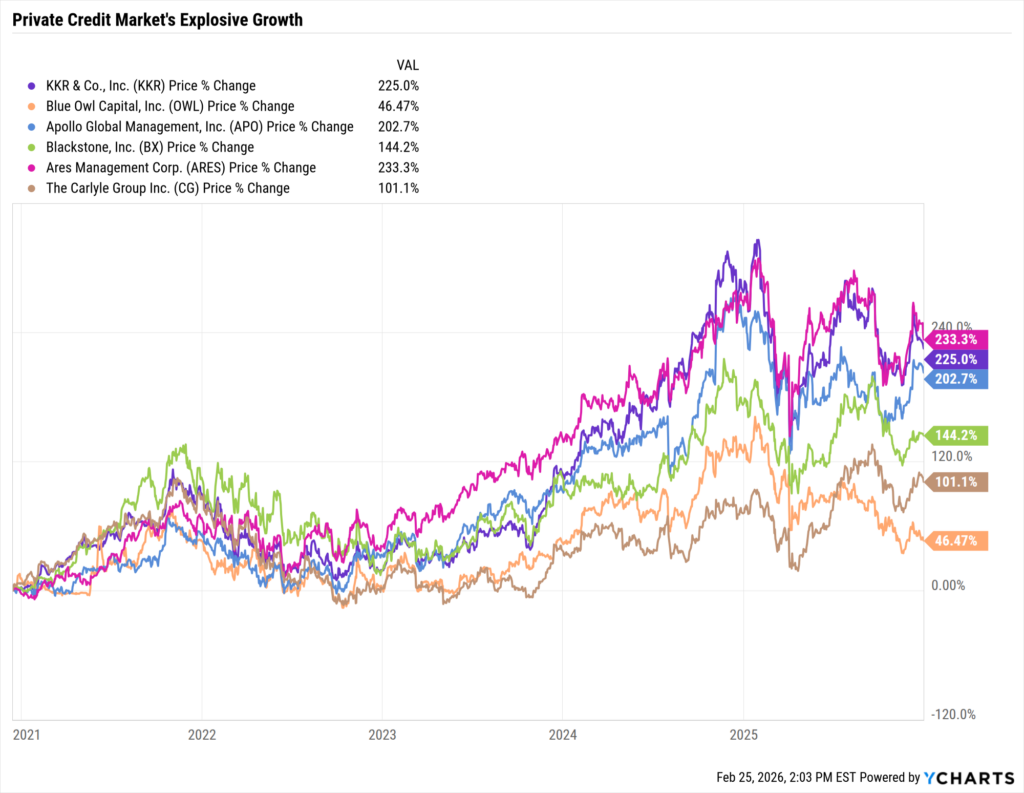

Private credit has been one of the most successful income engines of the past decade. It is also now large enough that structural decisions, particularly around redemptions, can move markets.

Those two realities are colliding.

Blue Owl Capital’s decision to sell $1.4B of loans and permanently halt redemptions in one retail-accessible vehicle triggered renewed comparisons to 2007. This is not a story about whether private credit has worked. It has. The question is whether this moment represents a structural break or a liquidity event inside a maturing asset class.

Interested in testing out YCharts for free?

Start 7-Day Free TrialTable of Contents

What Happened With Blue Owl and Why It Mattered

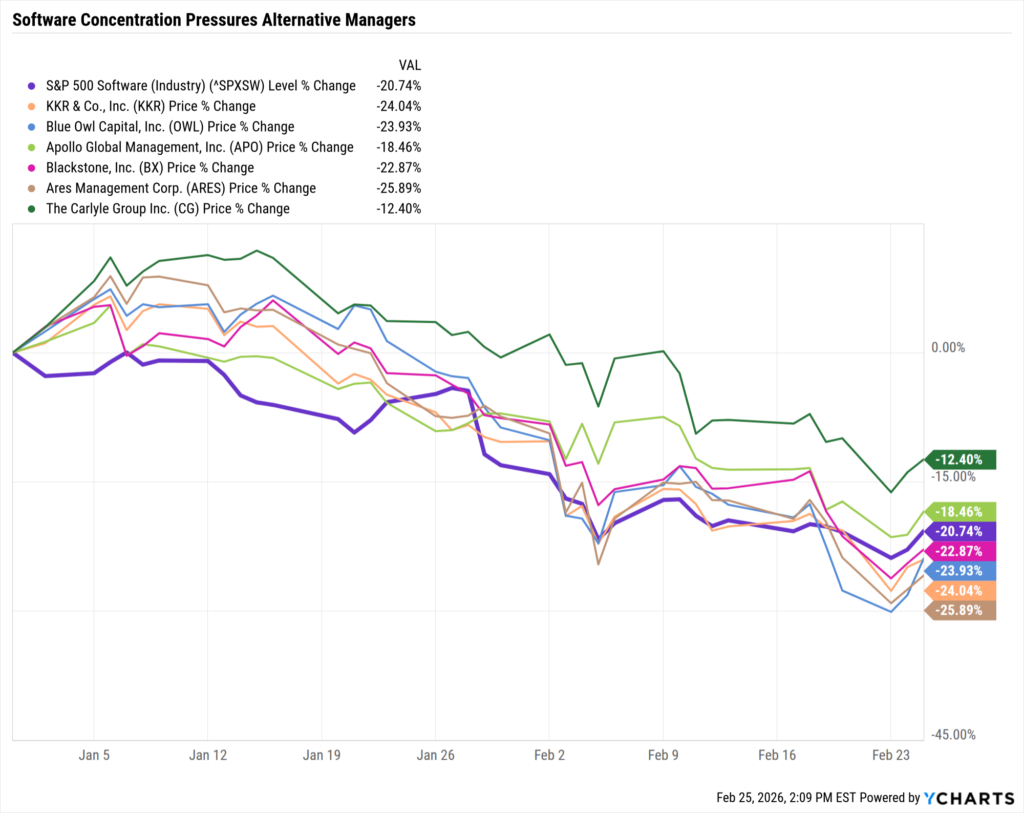

Blue Owl announced it would sell approximately $1.4B in loans from three credit funds to return capital and reduce leverage. The transaction reportedly cleared at roughly 99.7% of par across 128 portfolio companies. Approximately 13% of the assets sold were tied to software-related borrowers.

The firm also permanently halted redemptions in OBDC II, its non-traded business development company designed for retail and high net worth investors. OBDC II lends primarily to middle-market companies and offers periodic, but limited, liquidity. The redemption halt reflects the mechanics of a semi-liquid structure under pressure, not an immediate wave of credit losses.

This reflects balance sheet and redemption mechanics, not an immediate surge in credit losses.

Why Markets Reacted

Private credit has often been positioned as stable, income-generating, and less volatile than public credit. That positioning depends on two assumptions holding simultaneously:

- Valuations are credible

- Liquidity terms align with underlying assets

A semi-liquid vehicle offering periodic redemptions while holding private loans introduces structural tension during periods of elevated withdrawal requests. When redemption activity rises, managers must sell assets, draw on facilities, limit withdrawals, or restructure capital.

At the same time, sector concentration amplified the reaction. Software has been one of the largest allocations within private credit portfolios over the past decade. The sector benefited from recurring revenue models, strong sponsor activity, and elevated growth multiples. As public software valuations compressed and refinancing conditions tightened, investors began reassessing leverage assumptions and exit pathways across private portfolios.

The combination of visible liquidity stress and shared software exposure prompted investors to reprice liquidity, governance, and concentration risk across the broader private credit industry.

That is why the event resonated beyond a single manager.

Why 2007 Comparisons Are Resurfacing

The comparison centers on two structural concerns: liquidity mismatch and valuation opacity.

Semi-liquid vehicles offer periodic redemptions while holding loans that cannot be quickly sold without discounts. When withdrawals rise, managers must sell assets, borrow, gate redemptions, or restructure capital. That dynamic resembles early stress patterns seen in prior cycles.

Private loans are not marked to market daily. In stable periods that dampens volatility. In stressed periods it shifts focus to valuation governance and incentive alignment.

A true 2007-style unwind would require:

- Excess system-wide leverage

- Broad covenant deterioration

- Accelerating defaults

- Forced asset liquidation

So far, those indicators appear mixed rather than extreme. The rhetoric is running ahead of the data.

The Bull Case for Private Credit Remains

Allocators embraced private credit for structural reasons including floating-rate income support, senior-secured positioning, and direct underwriting flexibility. The asset class has scaled meaningfully, with Moody’s projecting global AUM approaching $3T by 2028. Over the past five years, private credit has outperformed many traditional fixed income segments.

One liquidity event does not invalidate a multi-year track record. Credit cycles tend to surface first in spreads and refinancing stress, not isolated redemption decisions.

The Bear Case: What Actually Matters

Stripped to fundamentals, the risks cluster into four areas.

Liquidity and Fund Structure

The primary risk is structural. Semi-liquid vehicles offer periodic redemptions while holding private loans that cannot be quickly liquidated without discounts. Investors should evaluate redemption terms, gating provisions, the use of fund-level leverage, and reliance on credit facilities. In stressed environments, liquidity mechanics matter as much as credit quality.

Underwriting Discipline

Late-cycle conditions can pressure underwriting standards. Spread compression, higher entry leverage, weaker covenants, and increased use of PIK structures can reduce margin for error. The key question is not whether defaults are rising today, but whether underwriting assumptions were built for a different rate and growth environment.

Concentration Risk

Sector clustering, particularly in software and AI-adjacent industries, has drawn scrutiny as public market repricing tightens refinancing conditions. Concentrated exposure can amplify stress if capital markets remain selective.

Bank Interconnectedness

Private credit funds often maintain lending relationships or liquidity facilities with banks. While indirect, these linkages create potential transmission channels that regulators are monitoring closely.

How to Speak to Clients Without Fear or Complacency

Step 1: Reframe the headline

“This is less about one manager and more about how semi-liquid structures behave when redemptions rise. It is a liquidity and structure discussion, not evidence of systemic credit deterioration.”

Step 2: Differentiate product structures

Private credit is not a single asset class. Public BDCs, non-traded BDCs, interval funds, drawdown vehicles, and evergreen funds operate under different liquidity, leverage, and valuation mechanics. Risk must be evaluated at the vehicle level.

Step 3: Anchor the discussion in disciplined due diligence

- How does the portfolio perform under widening spreads or refinancing stress?

- What are the precise redemption terms and gating provisions?

- What portion of the portfolio could realistically be sold within 30 days?

- How are valuations determined and independently reviewed?

- What is the fund-level leverage profile and covenant protection?

- Where is concentration risk by sector, sponsor, or vintage?

Step 4: Align liquidity expectations

If a client requires liquidity certainty, private credit should be sized as capital that may not be immediately accessible, regardless of periodic redemption language.

The Bottom Line for Advisors

Private credit is not automatically “the next 2008,” but the Blue Owl episode is a useful stress test of what matters most in private markets: liquidity plumbing, valuation governance, and investor suitability. The right advisor posture is neither panic nor complacency. It is segmentation (who should own it), structure literacy (what clients actually bought), and process (how you monitor risk as the cycle turns).

Ready to Move On From Your Investment Research and Analytics Platform?

Sign up for a copy of our Fund Flows Report: to keep tabs on flows into ETFs and Mutual Funds:

Sign up for our free monthly Fund Flow Report:Follow YCharts Social Media to Unlock More Content!

Next Article

3 Ways National Accounts Teams Can Strengthen Platform RelationshipsRead More →