Economic Update — Reviewing Q3 2022

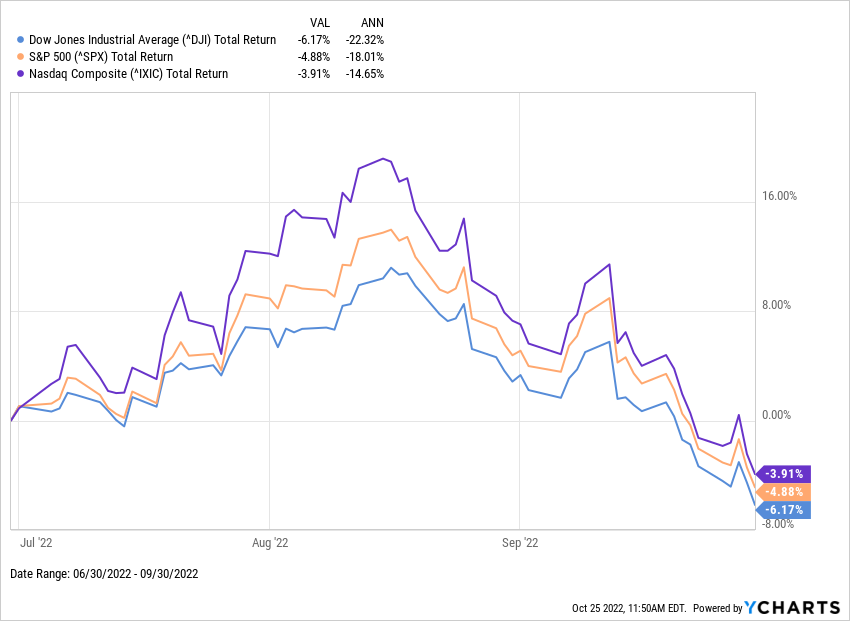

US Stocks continued their downward slide in Q3 of 2022, marking three consecutive quarters in the red for all three major equity indices. The Dow Jones Industrial Average fell the hardest with a 6.17% decline in the third quarter, followed closely by the S&P 500 and Nasdaq Composite.

Download Visual | Modify in YCharts

Below is a sneak peek of insights from the YCharts Q3 2022 Economic Summary Deck. The deck, published quarterly, arms advisors and investors with key insights from the previous quarter to help you make smarter investment decisions going forward. The deck is also easily customizable with your own firm branding to be leveraged in client communications.

Want the Economic Update slide deck sent straight to your inbox? Get it here:

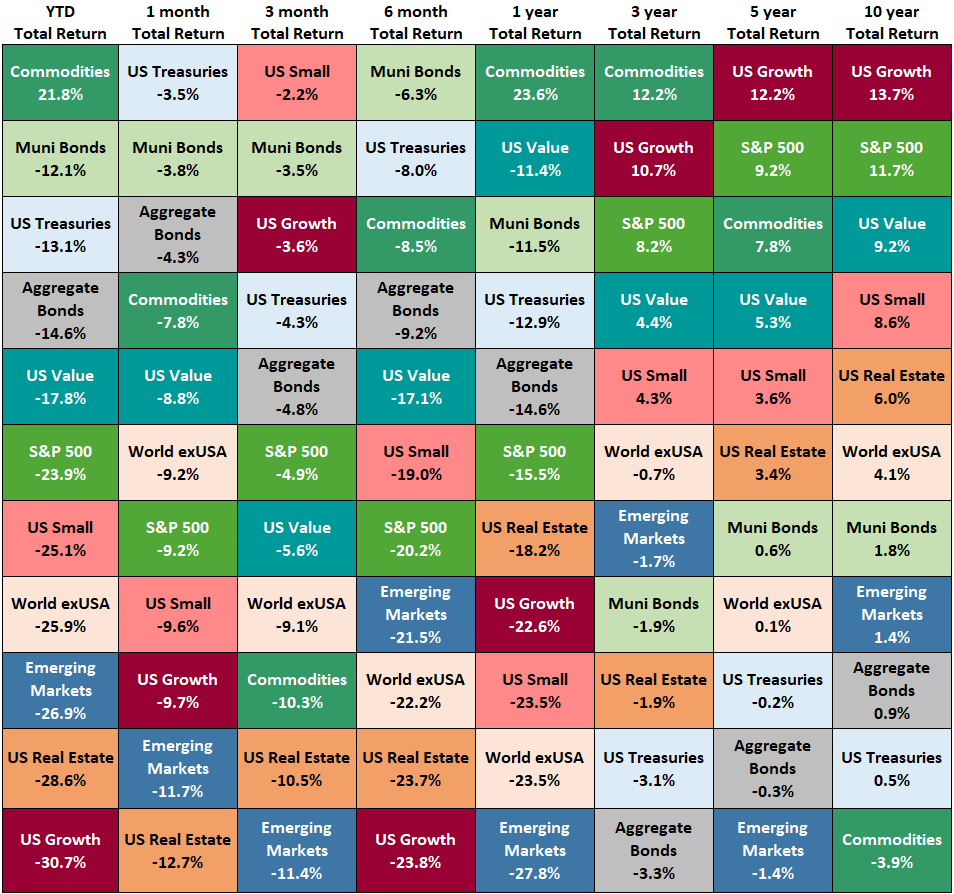

Asset Class Performance

The table below shows the performance of asset classes over increasingly longer lookback periods.

Click to Download Asset Class Performance Table

US Small Cap was the relative outperformer in Q3 2022 despite falling 2.2% in Q3. Meanwhile, Commodities are still leading year-to-date even after posting a -10.3% return in Q3. Emerging Markets took the biggest tumble in Q3 2022, down 11.4% over the quarter for a YTD decline of nearly 27%.

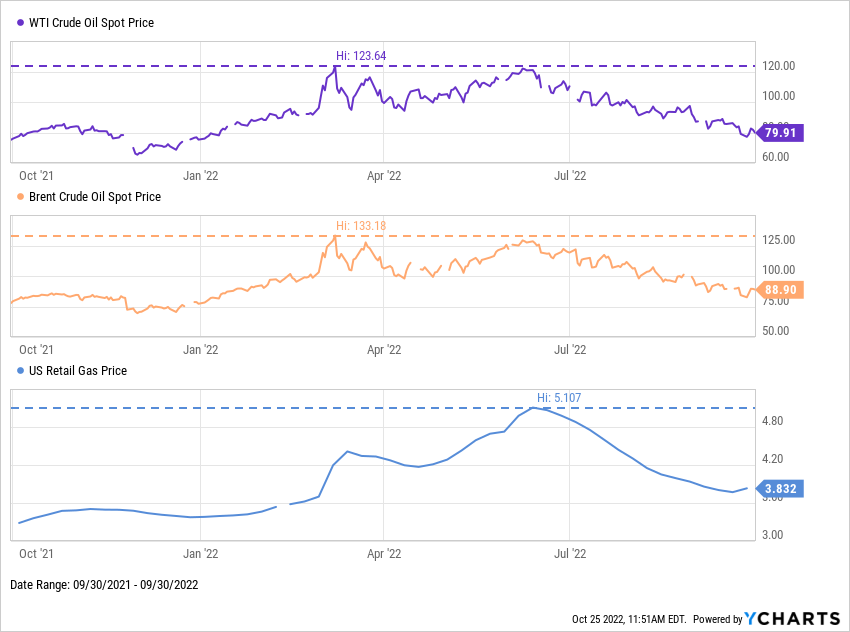

Easing Oil & Gas Prices

WTI & Brent Crude Oil hit highs in early 2022, causing drivers to feel the pinch at the pump. However, Q3 reversed those gains with each spot price decreasing by more than 25% and retail gas prices tracking accordingly.

Download Visual | Modify in YCharts

Inflation Adjusted Earnings

On a relatively positive note, Inflation rates haven’t increased this quarter, but year-over-year figures remain high. The Inflation Rate was 8.2% as of September, and Core Inflation logged a ten-year high of 6.63%.

Wage growth, illustrated by US Average Hourly Earnings, has for the most part consistently set all-time highs. However, bigger paychecks don’t necessarily translate to greater purchasing power as other inflation inputs have risen faster, resulting in Real Average Hourly Earnings that are now below pre-COVID levels.

YCharts users—download the entire deck in the Support Center. Not a current client? Reach out to get access, or enter your email below to receive a free version of the deck:

Get the Economic Update slide deck sent straight to your inbox:

Connect with YCharts

To get in touch, contact YCharts via email at hello@ycharts.com or by phone at (866) 965-7552

Interested in adding YCharts to your technology stack? Sign up for a 7-Day Free Trial.

Disclaimer

©2022 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts”) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure

Next Article

TSLA's Long Road Ahead, Bond Yields, US v. CAN | What's Trending on YCharts?Read More →