Highlights, Lowlights and Insights from 1H 2022

The first half of 2022 has been painful yet historic for stocks. Going back to 1950, the S&P 500’s -20.6% decline through two quarters this year is its third-worst start on record, behind only 1962 and 1970.

But as with most market storylines, a wider lens adds meaningful context. For example, while 78% of S&P 500 constituents are lower year-to-date in 2022, just 31% remain below their pre-COVID-19 highs from February 2020. Depending on the framing, the insight would equate to either a devastating first half, or a saving grace from stocks’ pullback in 2022.

Below are even more highlights, lowlights, and insights from 1H 2022. Together and individually, they use data to paint a picture of where the market has been, and where it might go later this year. All visuals can be downloaded for your use.

S&P 500, Dow 30, and Nasdaq 100 Insights from 1H 2022:

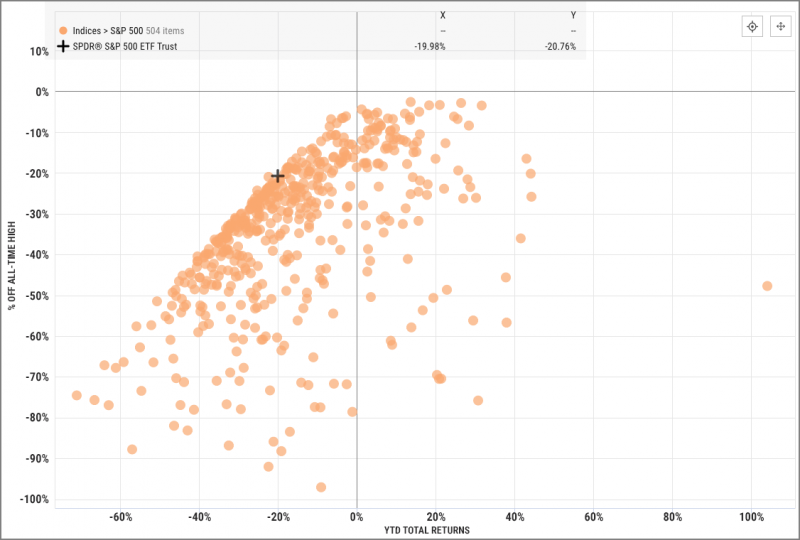

S&P 500

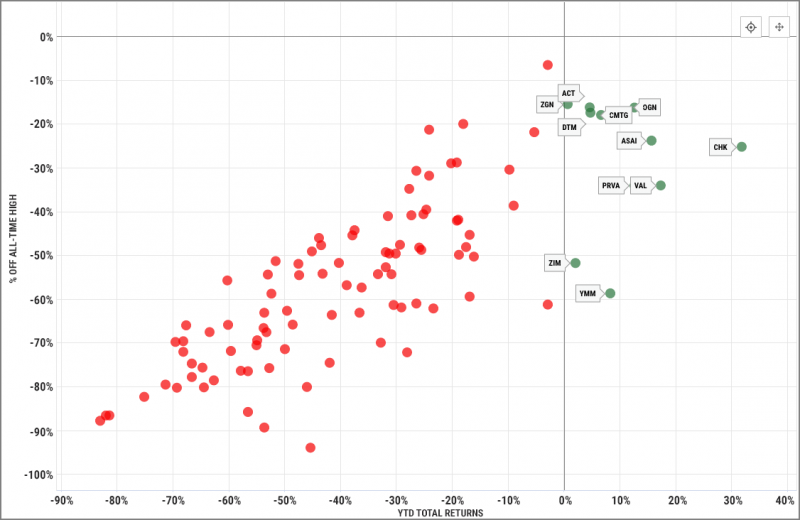

Through the first half of 2022, 78% of all S&P 500 constituents (394 individual names) posted negative year-to-date returns while 22% (108 constituents) were up YTD. The more positive spin is that 69%, or 346 stocks, remain higher than their pre-COVID-19 levels from February 18, 2020.

Download Visual | Modify in YCharts

With YTD Total Returns on the x-axis and Percent Off All-Time High on the y-axis, this Scatter Plot reveals a strong 1:1 relationship between the two metrics, due to most S&P 500 stocks setting their all-time highs on or around January 3, 2022.

The S&P 500’s Biggest 1H 2022 Winners:

Occidental Petroleum Corp (+104.0%)

Valero Energy (+44.3%)

Hess Corp (+44.1%)

The S&P 500’s Biggest 1H 2022 Losers:

Netflix (-71.0%)

Etsy (-66.6%)

Align Technologies (-64.0%)

View Key Stats for All S&P 500 Stocks in 1H 2022

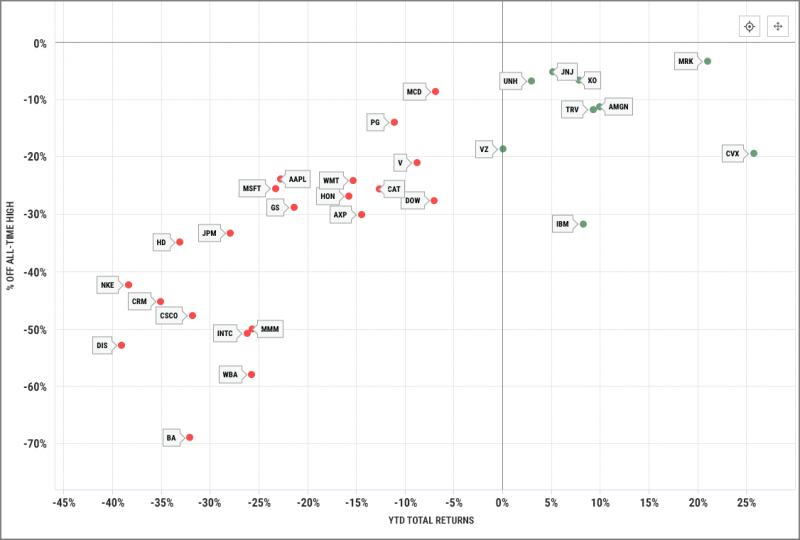

Dow Jones Industrial Average

21 of the 30 names in the Dow Jones Industrial Average are negative through the first half of 2022, with just nine names, or 30% of the index, higher through two quarters. Similarly to the S&P 500, that stat flips when pegging returns to the COVID-19 crash, with all but ten Dow-30 stocks below their February 18, 2020 levels.

Download Visual | Modify in YCharts

The Dow Jones’ Biggest 1H 2022 Winners:

Chevron Corp (+25.7%)

Merck & Co (+21.0%)

Amgen Inc (+10.0%)

The Dow Jones’ Biggest 1H 2022 Losers:

The Walt Disney Co (-39.1%)

Nike Inc (-38.4%)

Salesforce Inc (-35.1%)

View Key Stats for All Dow Jones Stocks in 1H 2022

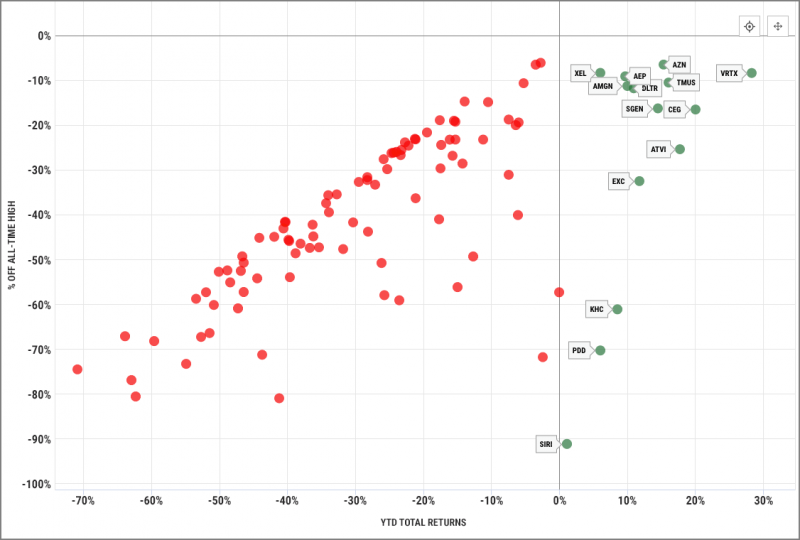

Nasdaq 100

Beat up worst of the three major stock averages, only 14 constituents of the Nasdaq 100 index, or 14%, are up after the first half of 2022. As a bright spot for the tech and growth-heavy Nasdaq, only 31 individual names are still below their February 18, 2020 levels.

Download Visual | Modify in YCharts

The Nasdaq 100’s Biggest 1H 2022 Winners:

Vertex Pharmaceuticals (+28.3%)

Constellation Energy Corp (+20.0%)

Activision Blizzard (+17.7%)

The Nasdaq 100’s Biggest 1H 2022 Losers:

Netflix (-71.0%)

Align Technology (-64.0%)

PayPal Holdings (-63.0%)

View Key Stats for All Nasdaq 100 Stocks in 1H 2022

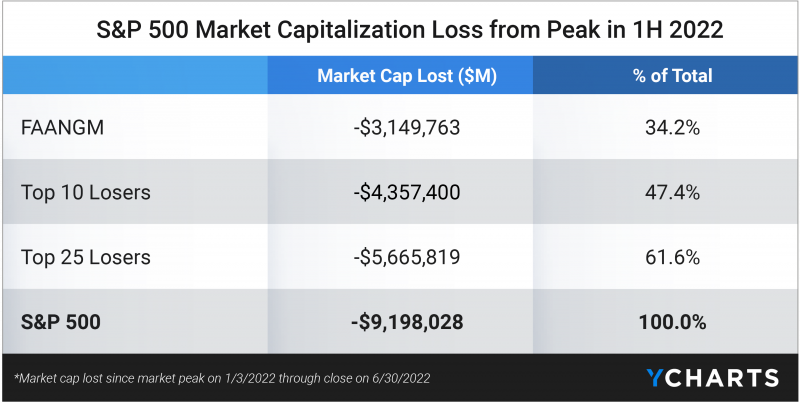

How Has “FAANGM” Contributed to Market Cap Losses in 2022?

After peaking on January 3rd, 2022, the S&P 500 lost an eye-watering $8.9 trillion of market capitalization by June 29th of the same year.

While it’s no secret that the S&P 500 is market cap-weighted, an outsized percentage of market cap losses can be attributed to its largest constituents. FAANGM stocks (Meta Platforms, Apple, Amazon, Netflix, Alphabet, and Microsoft) are responsible for a combined $3.0 trillion of lost market cap, while the index’s top 25 losers—still just 5% of all names in the index—contributed 61.5% of market cap losses in the first half of 2022.

Examining the S&P 500’s top 10 losers by market capitalization, Apple, Amazon, Microsoft, and Tesla (TSLA) have been leading the index lower.

Free Whitepaper: The Real Impact of Mega Cap Stocks on Your Portfolio & The Market: Examining Examining How Much Our Wealth Is Intertwined with The Performance—and Risks—of A Handful of Companies Including Apple, Amazon, Microsoft, Tesla & Others

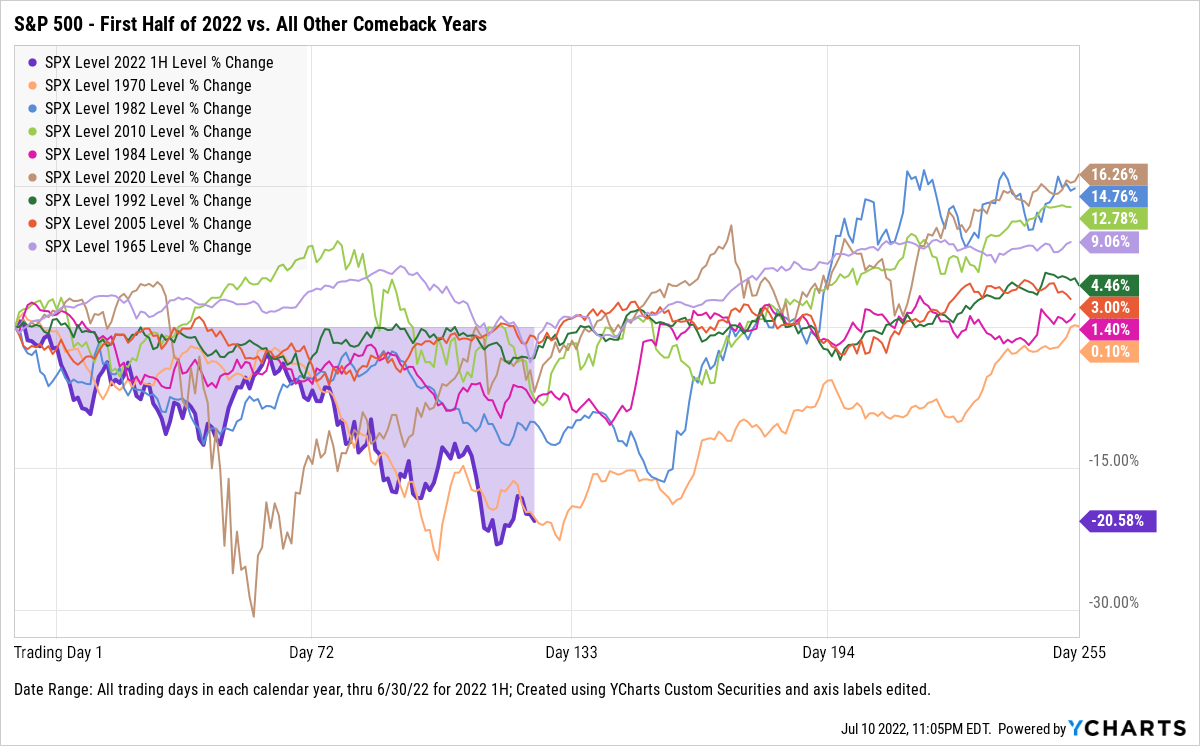

How Does 2022’s Slow First Half Compare to Others, Historically?

Since 1950, the S&P 500 has fallen in the first half of 23 calendar years (and risen in the first half of 50). Of those 23 years, the S&P completed a comeback in just eight of them, the most recent of which came in 2020.

While going 8-for-23 means the S&P 500 has converted a negative 1H to a positive full-year 34.8% of the time, 2022 is the third-worst 1H since 1950 for the S&P 500, down 20.6% at the half. Only in 1970 did the index come back from such a poor start, a year in which the S&P finished 0.1% in the black.

The table below shows expanded data from the chart above. In 22 historical calendar years with negative 1H performance, the S&P 500’s average 1H return was -8.2% and its full-year average was -6.3%.

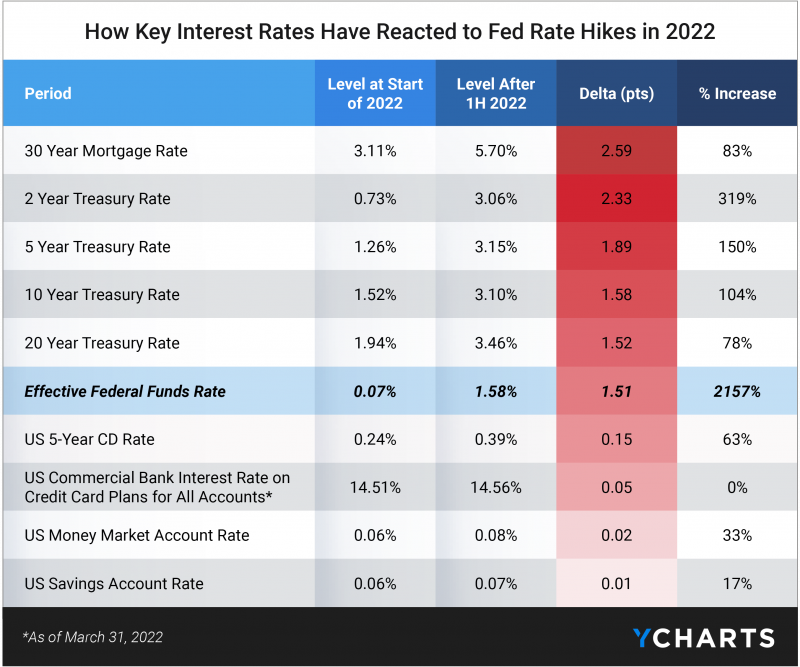

How Have Key Interest Rates Reacted to Fed Funds Rate Hikes in 2022?

The 30-year mortgage rate and short-term treasury rates have seen the largest impact from Fed Rate Hikes. Unfortunately, savings account, money market, and CD rates have not responded in kind.

Download Visual | View Data in YCharts

30 Year Mortgage Rate

2 Year Treasury Rate

5 Year Treasury Rate

10 Year Treasury Rate

20 Year Treasury Rate

Effective Federal Funds Rate

US 5-Year CD Rate

US Commercial Bank Interest Rate on Credit Card Plans for All Accounts

US Money Market Account Rate

US Savings Account Rate

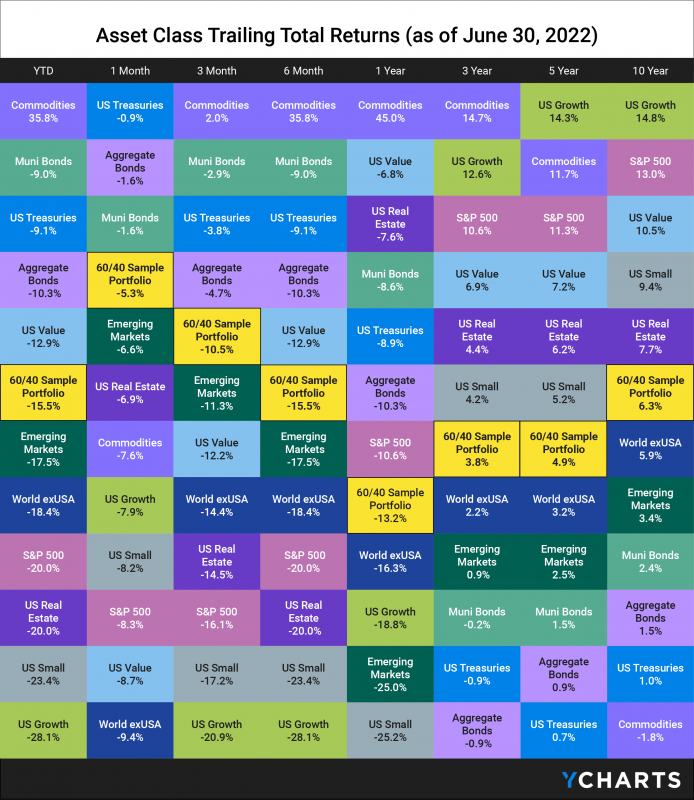

How Has the 60/40 Portfolio Fared Compared to Other Asset Classes in 2022?

While stocks have plunged in 2022, fixed income has been a relative brightspot for investors in ol’ reliable, the 60/40 Portfolio of 60% stocks and 40% bonds. Commodities are the sole positive-performing asset class of the year, topping the table below for a number of lookback periods, but Muni Bonds and US Treasuries each have limited YTD losses too under 10.0%.

The 2022 picture is more sour for previously high-flying asset classes, such as US Growth stocks, US Small Caps, and Real Estate. All solid performers over the last 10 years, the most recent six months provide an answer to, “what have you done for me lately?” …Nothing.

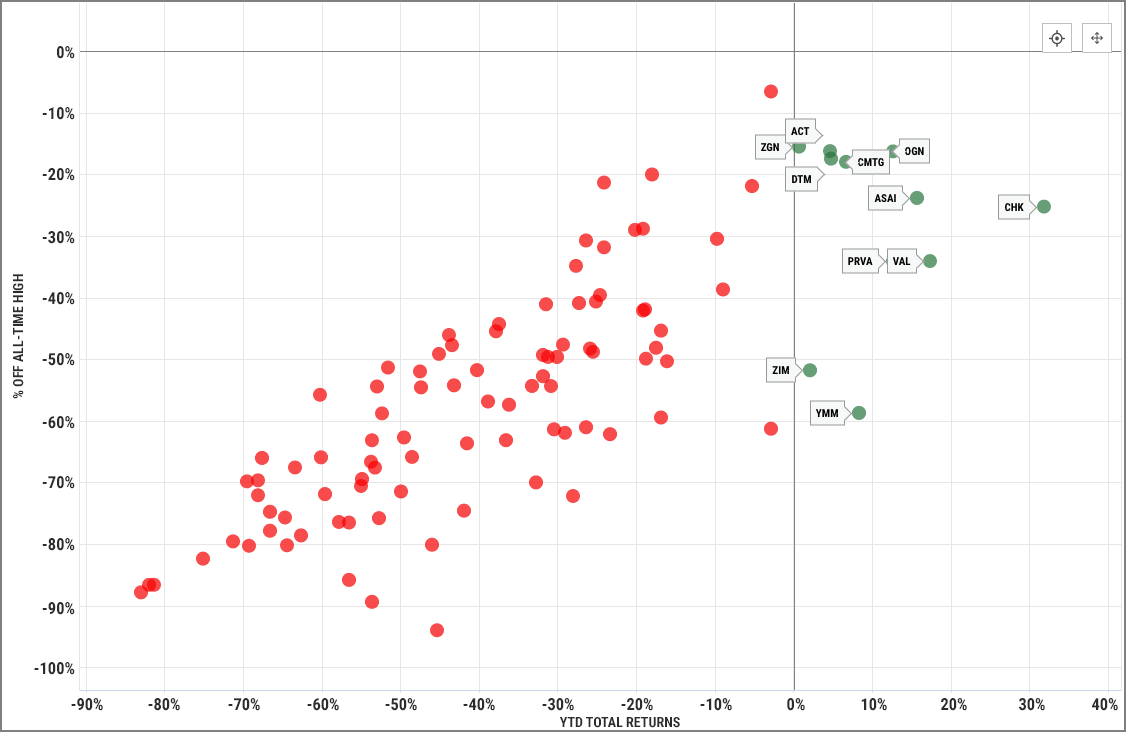

How Have 2021’s IPOs Held Up in 1H 2022? All IPOs Since the COVID-19 Crash?

It’s crazy to think that COVID-19 first brought the IPO market to a screeching halt in 2020. Then Special Purpose Acquisition Companies (SPACs), a faster and flashier alt-IPO, skyrocketed in 2021, and now IPO volume is back to near-record lows.

The first half of 2022 has been especially unkind to the newest publicly listed companies. Only 11 of 2021’s 100 largest IPOs (by current market cap) are positive year-to-date in 2022.

{kind=link}

IPOs from 2021 That Are Up Through 1H 2022:

Chesapeake Energy Corp (CHK)

Valaris Ltd (VAL)

Sendas Distribuidora SA (ASAI)

Privia Health Group Inc (PRVA)

Organon & Co (OGN)

Full Truck Alliance Co Ltd (YMM)

Claros Mortgage Trust Inc (CMTG)

DT Midstream Inc (DTM)

Enact Holdings Inc (ACT)

ZIM Integrated Shipping Services Ltd (ZIM)

Ermenegildo Zegna NV (ZGN)

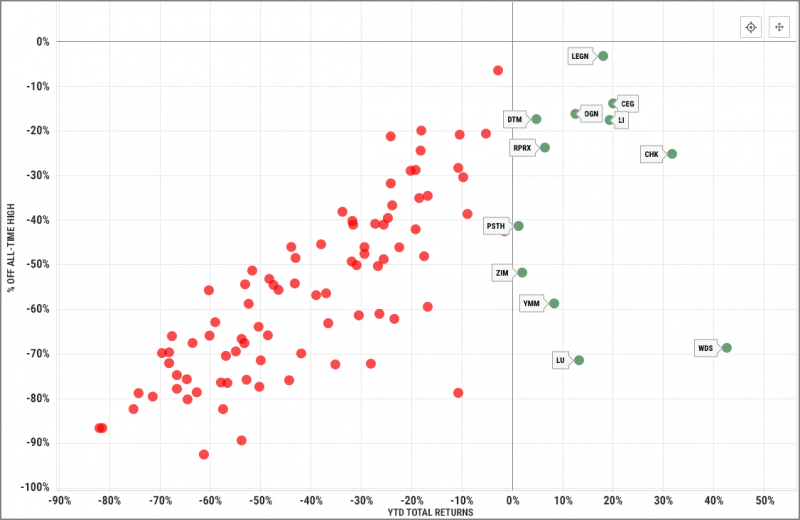

Only 12 of the 100 largest IPOs (by current market cap) since the COVID-19 Crash began are positive year-to-date in 2022.

IPOs Since COVID Crash in 2020 That Are Up Through 1H 2022:

Woodside Energy Group Ltd (WDS)

Chesapeake Energy Corp (CHK)

Constellation Energy Corp (CEG)

Li Auto Inc (LI)

Legend Biotech Corp (LEGN)

Lufax Holding Ltd (LU)

Organon & Co (OGN)

Full Truck Alliance Co Ltd (YMM)

Royalty Pharma PLC (RPRX)

DT Midstream Inc (DTM)

ZIM Integrated Shipping Services Ltd (ZIM)

Pershing Square Tontine Holdings Ltd (PSTH)

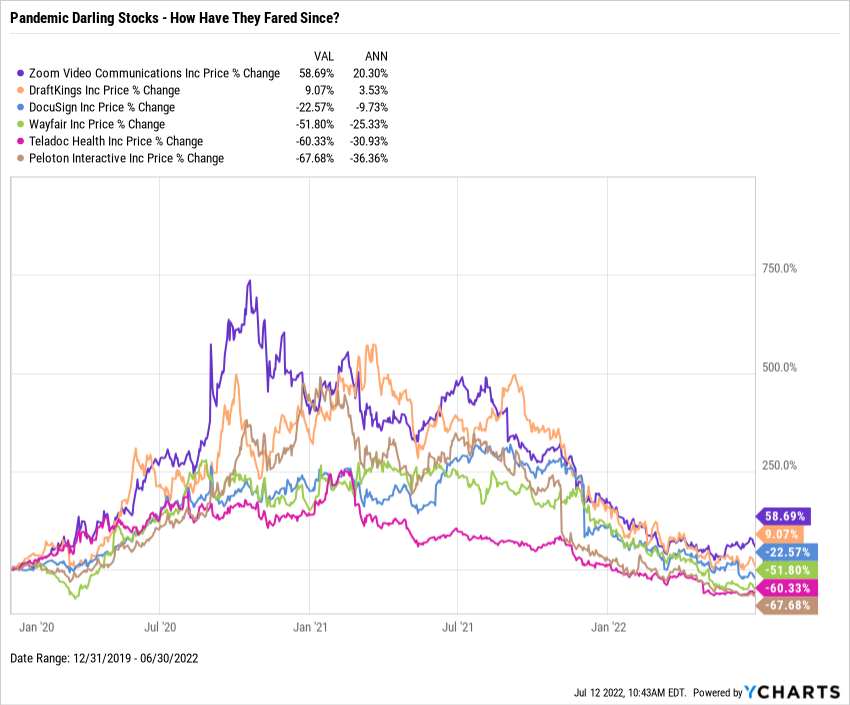

How Has 1H 2022 Treated Meme Stocks & Pandemic Favorites?

The short answer: not kindly.

While names like Zoom (ZM), DocuSign (DOCU), Peloton (PTON) and Teladoc (TDOC) were trending for the right reasons in 2020, “stay-at-home” stocks have floundered as most of us have returned to normalcy. Transitioning into a hybrid era in 2H 2022 and beyond, these businesses may still be solid, but perhaps just not at valuations seen in late 2020 and early 2021.

Download Visual | Modify in YCharts

AMC Entertainment (AMC) and Gamestop (GME), on the other hand, became meme-famous for reasons that raised a lot of eyebrows. When the internet banded together to squeeze out short-sellers, GME and AMC “went gamma” and have held onto a staggering amount of their new value since.

Are internet memes enough to resurrect a dead stock for good? Only time will tell.

Download Visual | Modify in YCharts

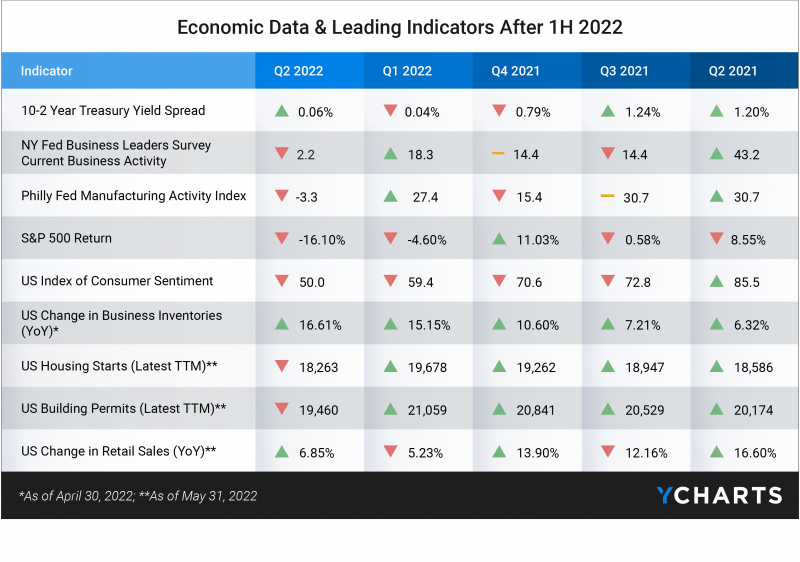

What Are Leading Economic Indicators Saying Beyond 1H 2022?

Naturally, you may now be asking, “What does the rest of 2022 have in store?”

According to well-followed leading indicators of economic growth, the back-half of the year does not look too rosy. Only the 10-2 Year Treasury Yield Spread, US Retail Sales YoY (as of May 31, 2022), and US Business Inventories YoY (as of April 30, 2022) point toward an improved economic picture in 2H 2022. Meanwhile, the Philly Fed Manufacturing Activity Index, NY Fed Business Leaders Survey, US Index of Consumer Sentiment, and S&P 500 quarterly returns are hinting at further struggles for the economy.

One spot of potential hope is that the economic slowdown has already been priced into stocks, and that any to-be-seen economic troubles won’t rock equity markets too badly. But, 2022 has already proved a lot of optimists wrong.

Download Visual | View Data in YCharts

Preparing for 2H 2022

The first half of the year has certainly delivered more lowlights than highlights, but “a smooth sea never made a skilled sailor,” as they say. If anything, advisors and investors can reflect on 1H 2022 and consider a few key takeaways:

First, the major averages and most of their constituents are down badly, but still above their pre-COVID-19 levels from little more than two years ago. Second, a well-balanced portfolio would have successfully limited the hemorrhaging in 2022, as in years past. And finally, the market has bounced back from worse starts (e.g. 1970), but we are currently digging ourselves out of quite the hole.

As discussed, framing and context have a lot of impact on the pictures we paint of the market. The right visuals, data points, or insights can make all the difference in emotions and behavior.

Connect with YCharts

To learn more, call us at (773) 231-5986, or email hello@ycharts.com.

Want to add YCharts to your technology stack? Sign up for a 7-Day Free Trial to see YCharts for yourself.

Disclaimer

©2022 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts”) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure.

Next Article

Record Gas Prices, $BRK Valuation, Income Fund Yields | What's Trending on YCharts?Read More →