Monthly Market Wrap: June 2026

Welcome back to YCharts’ Monthly Market Wrap, your data-driven recap of market trends shaping portfolios and client conversations. In June, small-cap and blue-chip stocks posted gains while the tech-heavy Nasdaq declined. Sector performance was evenly split, led by strong gains in Industrials and Health Care. Commodities fell sharply—particularly gold, silver, and oil—and Treasury yields were mixed, with short-term yields rising and long-term yields edging lower.

Want to use these visuals in your own presentations? Download our free Monthly Market Wrap slide deck, containing all charts featured in the Market Wrap and more in a shareable, presentation-ready format.

Market Summary: June Sees Mixed Index and Sector Performance as Commodity Prices Tumble

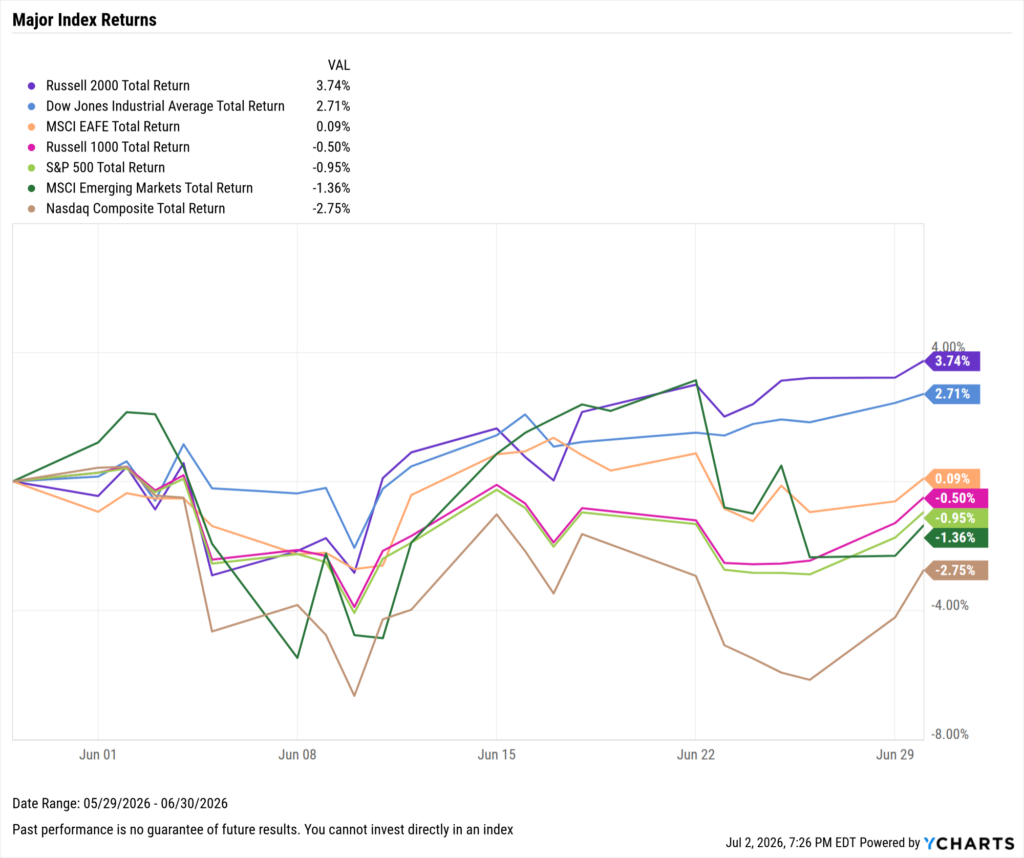

Markets were mixed in June. The small caps Russell 2000 led the way with a 3.7% gain, while the blue-chip Dow Jones Industrial Average posted a 2.7% increase. The tech-heavy Nasdaq was the largest laggard, slipping 2.8% in June.

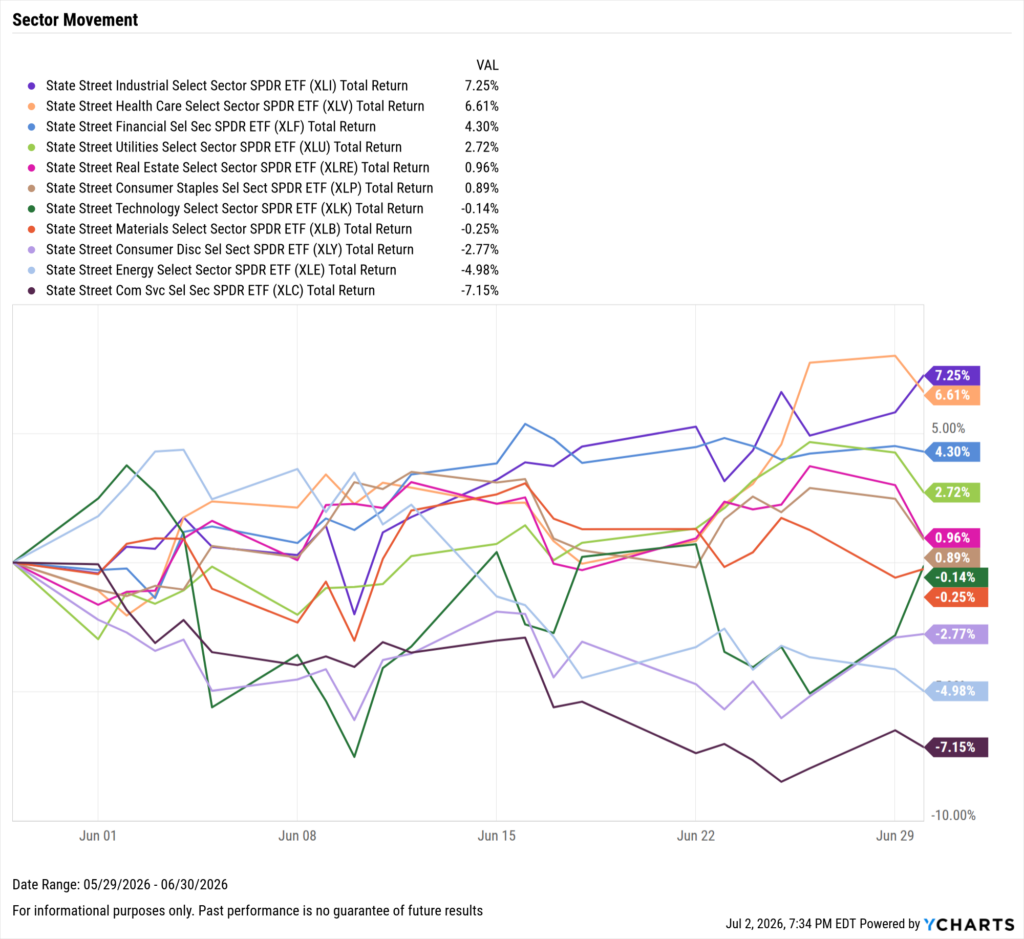

Sector performance was split fairly evenly, with six of the eleven sectors ending the month higher. Industrials led with a 7.3% gain, followed by Health Care rising 6.6%. Energy lagged for the third consecutive month, down 5.0%, with Communication Services logging the worst sector performance of 7.2% in June.

Commodity prices plummeted in June. The price of Gold slumped 11.7% in June, and 14.4% in Q2. The price of Silver fell even harder, down 21.8% in the month and 21.5% for the quarter. Oil price volatility continued in June, as the price of Brent crude tumbled 22.9% in the month, putting it 48% below its high set in early April. WTI ended June down 21.2%, and 37.3% below its recent high set three months ago.

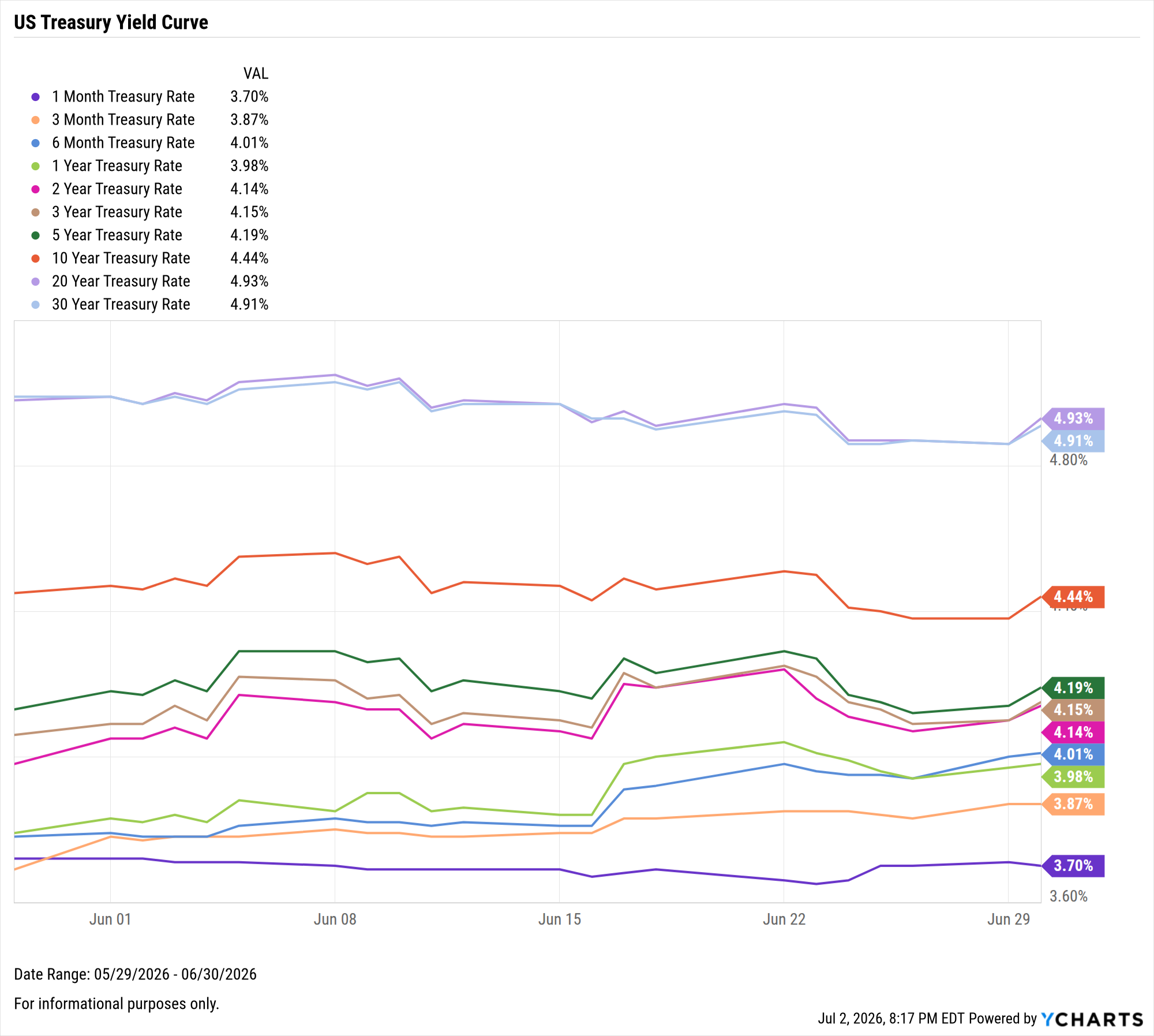

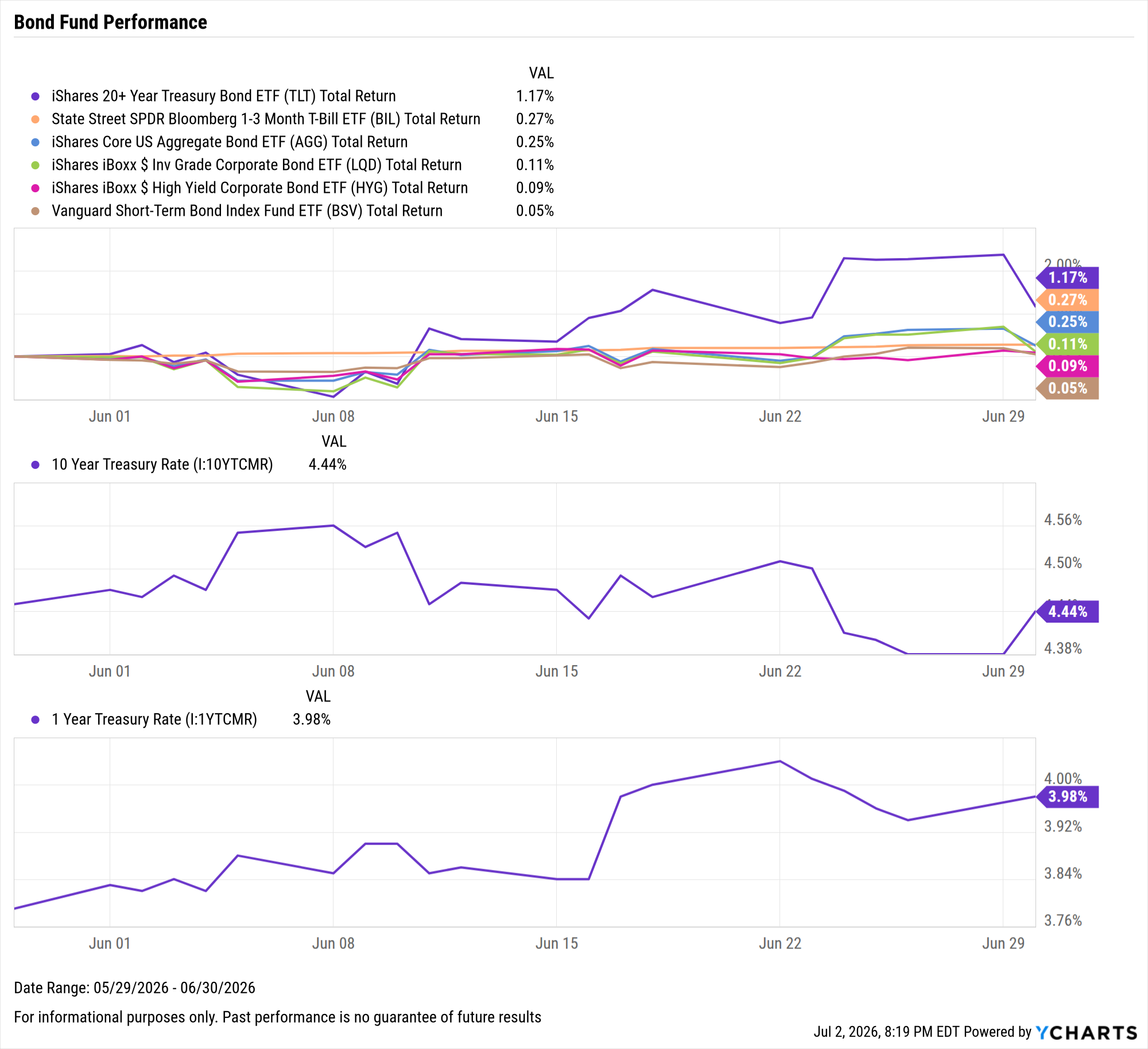

Treasury yields had mixed movements in June as yields on shorter-term treasuries increased while those of longer-term instruments decreased. The 3-month, 6-month, and 1-year rose 18, 23, and 19 basis points, respectively. The 20-year declined 5 basis points, and the 30-year slipped 8 bps. Bond funds were up across the board in June, as the iShares 20+ Year Treasury Bond ETF (TLT) led with a 1.2% gain.

Jump to Fixed Income Performance

Want to create your own monthly recap, complete with these charts in a presentation deck that contains your firm’s branding? Start a Free Trial →

Off the YCharts! Halftime Report

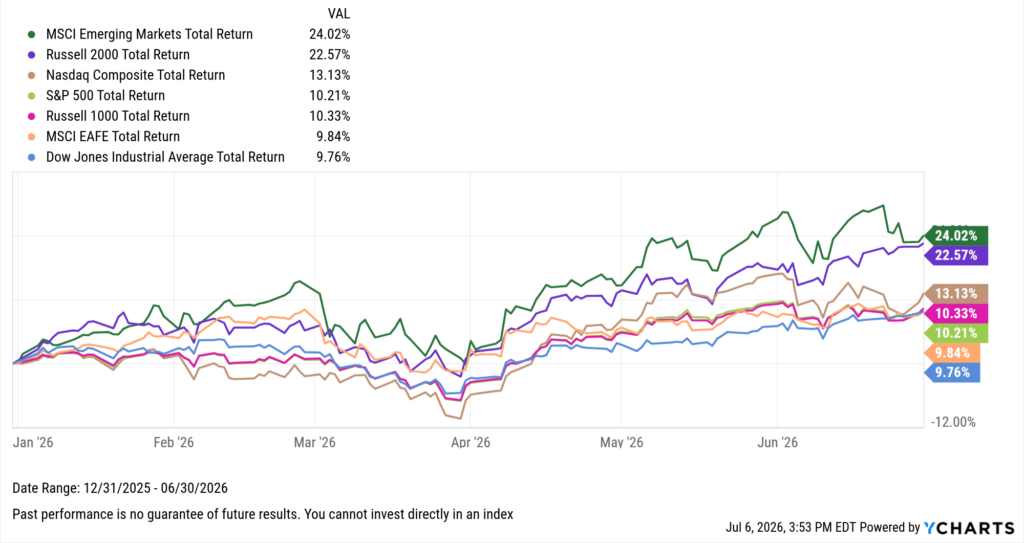

Six months into 2026, market leadership has broadened well beyond large-cap US equities for the second consecutive year.

Download Visual | Modify in YCharts

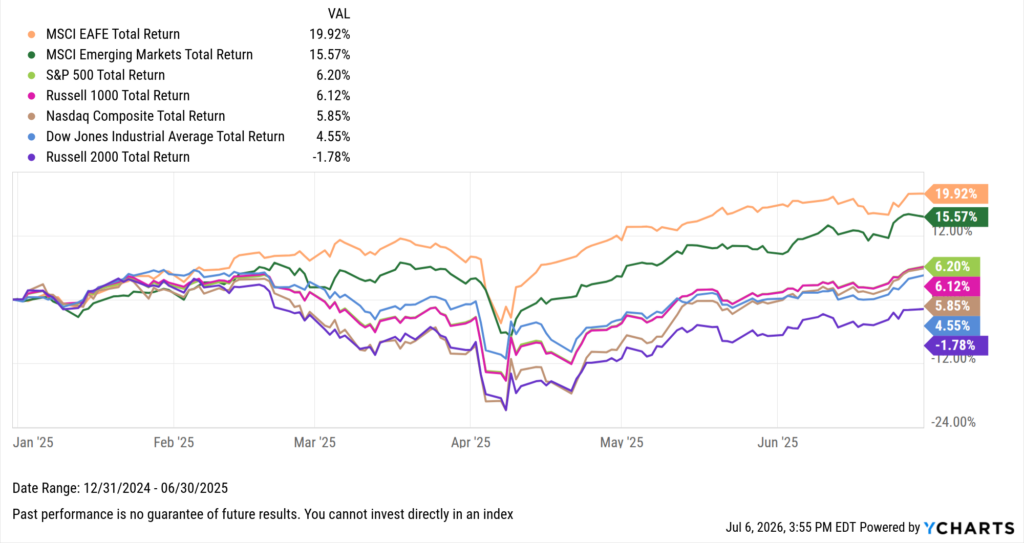

Emerging markets and small caps have led the way, up 24% and 22.6% respectively, both well ahead of the S&P 500’s 10.2% gain. At this point last year, the S&P had only increased by 6.2%, and would ultimately finish the year nearly 18% higher. All other major indices are positive by more than 9%.

Download Visual | Modify in YCharts

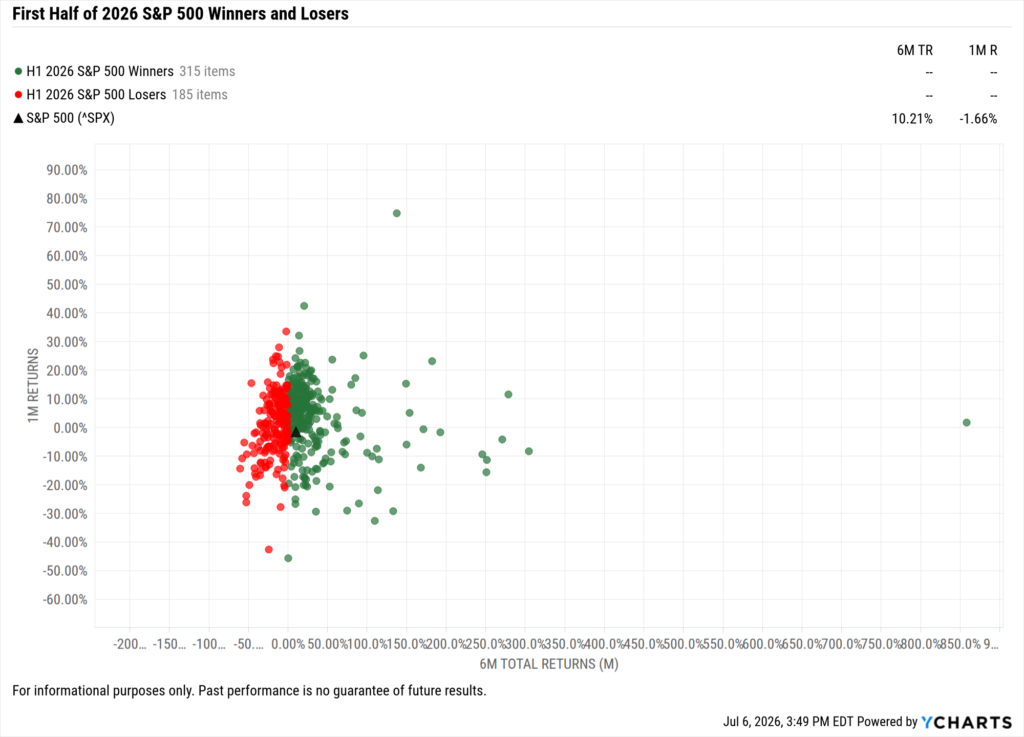

Breadth beneath the S&P 500 supports the broader participation story. Of the index’s 500 constituents, 315 posted positive six-month total returns against 185 decliners, with gains led by Sandisk, up more than 850%.

Download Visual | Modify in YCharts

Inflation remains the backdrop to watch. In May, the US inflation rate rose 0.40% month over month to 4.2%, the highest reading in three years and the third straight monthly increase. The Fed has now run above its 2% target for more than 5 years, and core PCE, which excludes food and energy prices, last fell below that threshold in February 2021.

For advisors, the H1 data points to a market rewarding a wider set of exposures than just large-cap US equities, with a persistently elevated inflation picture worth watching as we head into the back half of the year.

Equity Performance: Small Caps Lead as Tech-Heavy Nasdaq Lags, Industrials and Health Care Outperform while Energy and Communication Services Struggle

Major Indices

Download Visual | Modify in YCharts | View Below Table in YCharts

| Index | 1 Month Total Returns | 3 Month Total Returns | 6 Month Total Returns | 1 Year Total Returns |

|---|---|---|---|---|

| Russell 2000 | 3.74% | 21.49% | 22.57% | 40.78% |

| Dow Jones Industrial Average | 2.71% | 13.38% | 9.76% | 20.65% |

| MSCI EAFE | 0.09% | 11.08% | 9.84% | 20.80% |

| Russell 1000 | -0.50% | 15.14% | 10.33% | 22.02% |

| S&P 500 | -0.95% | 15.20% | 10.21% | 22.33% |

| MSCI Emerging Markets | -1.36% | 24.15% | 24.02% | 44.18% |

| Nasdaq Composite | -2.75% | 21.60% | 13.13% | 29.48% |

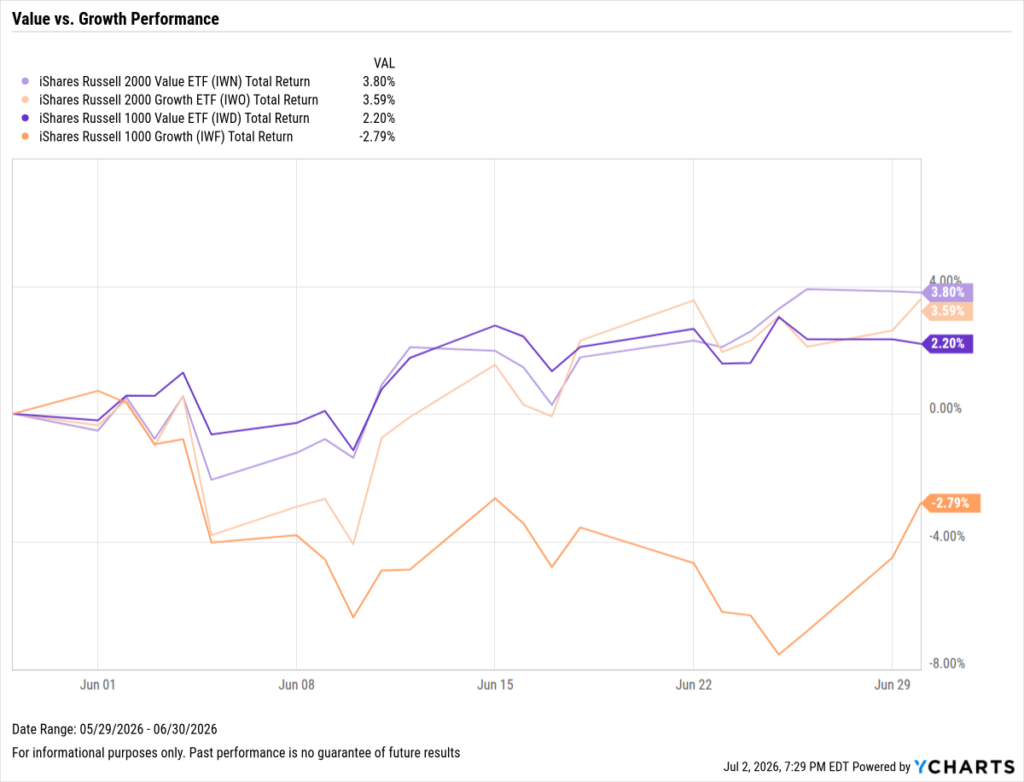

Value vs. Growth Performance

Download Visual | Modify in YCharts | View Below Table in YCharts

| Ticker | Name | 1 Month Total Returns | 3 Month Total Returns | 6 Month Total Returns | 1 Year Total Returns |

|---|---|---|---|---|---|

| IWN | iShares Russell 2000 Value ETF | 3.80% | 17.09% | 22.85% | 42.58% |

| IWO | iShares Russell 2000 Growth ETF | 3.59% | 25.69% | 22.14% | 38.49% |

| IWD | iShares Russell 1000 Value ETF | 2.20% | 13.81% | 16.05% | 26.86% |

| IWF | iShares Russell 1000 Growth | -2.80% | 16.58% | 5.12% | 17.41% |

US Sector Movement

Download Visual | Modify in YCharts | View Below Table in YCharts

| Ticker | Sector | 1 Month Total Returns | 3 Month Total Returns | 6 Month Total Returns | 1 Year Total Returns |

|---|---|---|---|---|---|

| XLI | Industrial | 7.25% | 14.81% | 20.04% | 27.17% |

| XLV | Health Care | 6.61% | 8.69% | 3.36% | 19.76% |

| XLF | Financial | 4.30% | 8.97% | -1.28% | 3.95% |

| XLU | Utilities | 2.72% | -0.57% | 7.62% | 14.12% |

| XLRE | Real Estate | 0.96% | 8.77% | 10.80% | 9.94% |

| XLP | Consumer Staples | 0.89% | 2.04% | 8.29% | 5.45% |

| XLK | Technology | -0.14% | 43.53% | 32.65% | 51.25% |

| XLB | Materials | -0.25% | 2.10% | 13.00% | 17.87% |

| XLY | Consumer Discretionary | -2.77% | 7.83% | -1.39% | 8.76% |

| XLE | Energy | -4.98% | -12.69% | 20.41% | 29.12% |

| XLC | Communication Services | -7.15% | -3.11% | -8.47% | -0.05% |

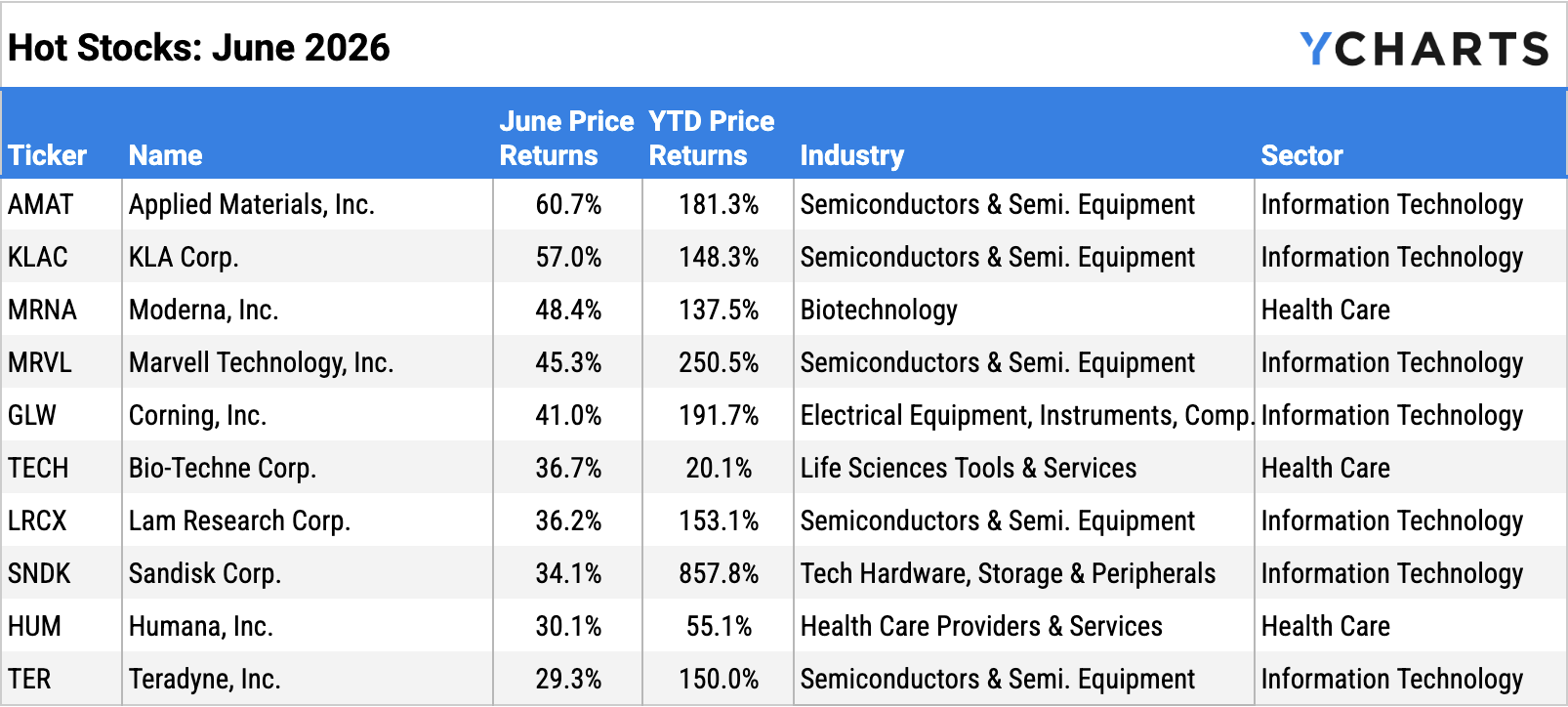

Hot Stocks: Top 10 S&P 500 Performers of June 2026

Download Visual | Modify in YCharts

| Symbol | Name | 1 Month Price Returns | YTD Price Returns | Industry | Sector |

|---|---|---|---|---|---|

| AMAT | Applied Materials, Inc. | 60.65% | 181.33% | Semiconductors & Semiconductor Equipment | Information Technology |

| KLAC | KLA Corp. | 57.00% | 148.30% | Semiconductors & Semiconductor Equipment | Information Technology |

| MRNA | Moderna, Inc. | 48.40% | 137.47% | Biotechnology | Health Care |

| MRVL | Marvell Technology, Inc. | 45.31% | 250.54% | Semiconductors & Semiconductor Equipment | Information Technology |

| GLW | Corning, Inc. | 41.00% | 191.72% | Electronic Equipment, Instruments & Components | Information Technology |

| TECH | Bio-Techne Corp. | 36.71% | 20.13% | Life Sciences Tools & Services | Health Care |

| LRCX | Lam Research Corp. | 36.19% | 153.14% | Semiconductors & Semiconductor Equipment | Information Technology |

| SNDK | Sandisk Corp. | 34.14% | 857.84% | Technology Hardware, Storage & Peripherals | Information Technology |

| HUM | Humana, Inc. | 30.06% | 55.09% | Health Care Providers & Services | Health Care |

| TER | Teradyne, Inc. | 29.26% | 149.97% | Semiconductors & Semiconductor Equipment | Information Technology |

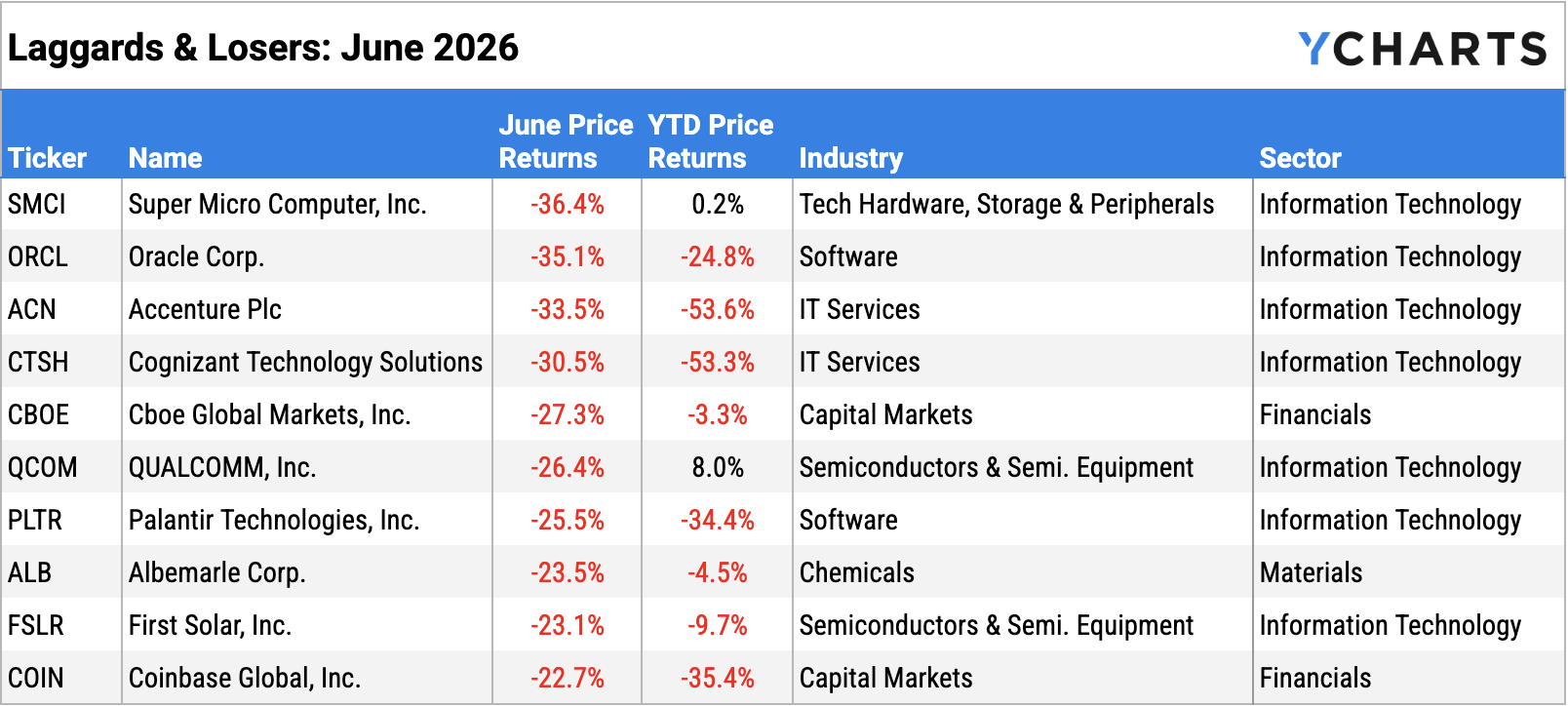

Laggards & Losers: 10 Worst S&P 500 Performers of June 2026

Download Visual | Modify in YCharts

| Symbol | Name | 1 Month Price Returns | YTD Price Returns | Industry | Sector |

|---|---|---|---|---|---|

| SMCI | Super Micro Computer, Inc. | -36.36% | 0.21% | Technology Hardware, Storage & Peripherals | Information Technology |

| ORCL | Oracle Corp. | -35.09% | -24.81% | Software | Information Technology |

| ACN | Accenture Plc | -33.48% | -53.62% | IT Services | Information Technology |

| CTSH | Cognizant Technology Solutions Corp. | -30.54% | -53.34% | IT Services | Information Technology |

| CBOE | Cboe Global Markets, Inc. | -27.25% | -3.32% | Capital Markets | Financials |

| QCOM | QUALCOMM, Inc. | -26.38% | 8.03% | Semiconductors & Semiconductor Equipment | Information Technology |

| PLTR | Palantir Technologies, Inc. | -25.47% | -34.36% | Software | Information Technology |

| ALB | Albemarle Corp. | -23.46% | -4.53% | Chemicals | Materials |

| FSLR | First Solar, Inc. | -23.09% | -9.67% | Semiconductors & Semiconductor Equipment | Information Technology |

| COIN | Coinbase Global, Inc. | -22.66% | -35.35% | Capital Markets | Financials |

Featured Market News and YCharts Insights

Meet Y: Your Specialized AI Agent

Why YCharts is the Best Investment Research Tool for Financial Advisors

Auto-Benchmarking in Model Portfolios: Accurate Benchmarks Without the Manual Work

Working the Core: Where Bond ETF Flows Are Heading in 2026

The 10 Best Performing REITs & REIT ETFs over the last 10 Years

Economic Data Overview: Inflation Reaches 3-Year High as Commodity Prices Plummet

Employment

The unemployment rate ticked down 0.1 percentage point to 4.2%, the lowest level in one year, and the U.S. economy added 57,000 jobs according to the most recent nonfarm payrolls report, well below the Dow Jones consensus forecast of 115,000. The US Labor Force Participation Rate decreased by 0.3 percentage points to 61.80%, reaching a five-year low.

Consumers and Inflation

The US inflation rate rose another 0.40% MoM to 4.2%, the highest reading since May 2023 and third straight monthly increase. Core inflation increased by 0.10% MoM to 2.90%, also logging its third monthly increase. The CME FedWatch tool indicates an 82% chance that the FOMC will hold the Fed Funds Rate at 3.50–3.75% during its next meeting on July 29th, with market pricing increasingly reflecting the possibility of a hike later in 2026.

Production and Sales

The US ISM Manufacturing PMI declined by 0.7 points to 53.30 for June after setting a three-year high of 54.00 in May. The Services PMI rose by 0.9 points in May to 54.50. The YoY US Producer Price Index surged higher for a fifth straight month straight to 6.5% in May, its highest reading since December 2022, while US Retail and Food Services Sales continued to increase, at 0.88% in May.

Housing

Existing Home Sales increased 3.22% MoM in May, while the Median Sales Price of Existing Homes reached a new all time high of $429,300, an increase of 2.83%, or $11,800, MoM.

Mortgage rates went virtually unchanged in June, ending the month at 5.84% for the 15-year and 6.49% for the 30-year, both as of June 25th. US New Single-Family Home Sales declined MoM, falling 7.35% in May, though well off the pace of January’s historic 20% drop.

Commodities

The price of Gold tumbled in June, with SPDR Gold Shares (GLD) plummeting 11.7% to end the month at $368.38 per share. Gold fell 14.4% in Q2. Silver fared even worse in June, as the iShares Silver Trust (SLV) tumbled 21.8% in the month and 21.5% for Q2.

Oil prices remained top of mind in June, though a fragile ceasefire framework between the US and Iran eased a significant amount of pressure on prices. Brent crude finished the month at $71.59, down 22.9% in June and 48% below the high of $138.21 set in early April. WTI ended June down 21.2% at $71.87 per barrel, 37.3% below the recent high of $114.58 it also reached in early April. The lower oil prices helped motorists feel relief at the pump, with the US Retail Gas Price falling 48 cents since the start of the month rising to $3.96 per gallon in June.

Cryptocurrencies

Major cryptocurrencies plummeted in June, following a down May. Bitcoin fell 18.4% to $60,159.63 per coin, while Ethereum declined more sharply, dropping 20.3% to $1,609.67.

Fixed Income Performance: Insights into Bond ETFs and Treasury Yields

US Treasury Yield Curve

1 Month Treasury Rate: 3.70%

3 Month Treasury Rate: 3.87%

6 Month Treasury Rate: 4.01%

1 Year Treasury Rate: 3.98%

2 Year Treasury Rate: 4.14%

3 Year Treasury Rate: 4.15%

5 Year Treasury Rate: 4.19%

10 Year Treasury Rate: 4.44%

20 Year Treasury Rate: 4.93%

30 Year Treasury Rate: 4.91%

Download Visual | Modify in YCharts

Bond Fund Performance

Download Visual | Modify in YCharts | View Below Table in YCharts

| Ticker | Name | 1 Month Total Returns | 3 Month Total Returns | 6 Month Total Returns | 1 Year Total Returns |

|---|---|---|---|---|---|

| TLT | iShares 20+ Year Treasury Bond ETF | 1.17% | 0.85% | 1.03% | 2.40% |

| BIL | State Street SPDR Bloomberg 1-3 Month T-Bill ETF | 0.27% | 0.88% | 1.74% | 3.83% |

| AGG | iShares Core US Aggregate Bond ETF | 0.25% | 0.72% | 0.74% | 3.79% |

| LQD | iShares iBoxx $ Inv Grade Corporate Bond ETF | 0.11% | 1.26% | 0.88% | 4.10% |

| HYG | iShares iBoxx $ High Yield Corporate Bond ETF | 0.09% | 2.05% | 1.69% | 5.15% |

| BSV | Vanguard Short-Term Bond Index Fund ETF | 0.05% | 0.38% | 0.51% | 2.98% |

Monitor the most important trends for clients as markets begin the second half of 2026. Download the visual aids directly from YCharts, and contact us for customized access to these charts.

Have a great July! 📈

Whenever you’re ready, there are three ways YCharts can help you:

1. Looking for a tool to help you better communicate market events?

Email us at hello@ycharts.com or call (866) 965-7552. You’ll be directly in touch with one of our Chicago-based team members.

2. Want to test out YCharts for free?

Start a no-risk 7-Day Free Trial.

3. Download a copy of the Monthly Market Wrap slide deck:

Disclaimer

©2026 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts”) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure

Next Article

YCharts Monthly Product Update: June 2026Read More →